Morgan Stanley: The U.S. September CPI is expected to rise again as tariff transmission continues to push up core inflation

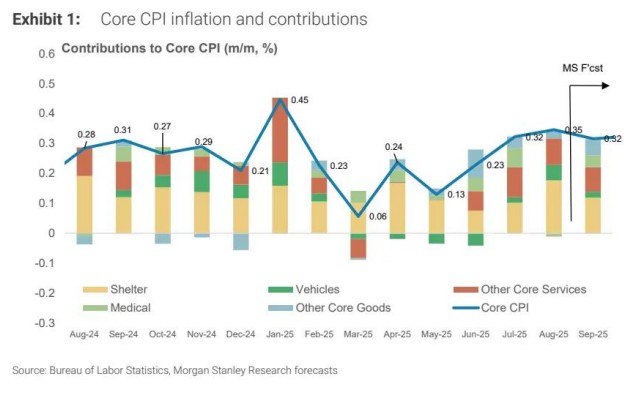

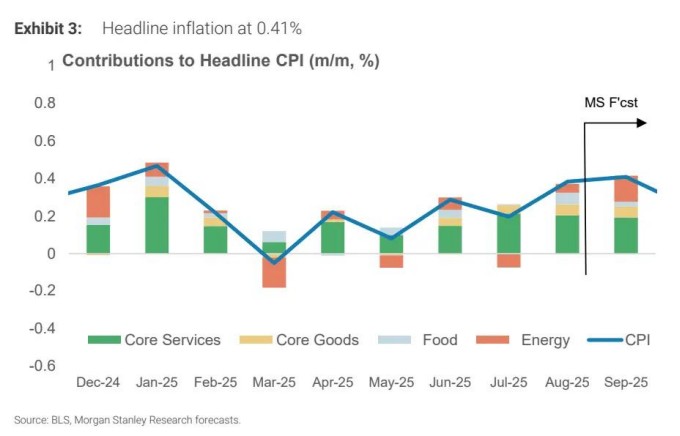

Morgan Stanley expects that the U.S. Consumer Price Index (CPI) for September will show that core CPI remains elevated, with overall inflation slightly higher than core inflation. Affected by tariff costs and rising energy prices, the core CPI increased by 0.32% month-on-month in September, with a year-on-year increase of 3.12%. The overall CPI rose by 0.41% month-on-month, mainly due to the rebound in energy prices. Food price inflation has slowed, with an expected month-on-month increase of 0.19%. Key observation points include the slowing transmission speed of tariffs and the continued inflation of auto insurance

According to Zhitong Finance APP, Morgan Stanley stated that due to the gradual transmission of tariff costs and rising energy prices, the U.S. Consumer Price Index (CPI) report for September, scheduled to be released on October 24, is expected to show that core CPI remains high, with overall inflation slightly above core inflation, while price trends in sub-sectors such as rent and medical services show divergence.

The bank predicts that the core CPI will rise by 0.32% month-on-month in September, with a year-on-year increase of 3.12%. This means that core goods inflation has remained positive for the fourth consecutive month, mainly due to the gradual transmission of tariff-related costs to consumers. Morgan Stanley estimates that tariff transmission has contributed approximately 25-30 basis points to the year-on-year core CPI this year. If this data meets expectations, this contribution will expand to 35 basis points, approaching half of its expected total tariff impact (assuming tariffs remain at current levels).

Overall inflation performance is expected to be stronger than core inflation. The bank forecasts that the overall CPI will rise by 0.41% month-on-month in September, higher than the core CPI increase, primarily due to a significant rebound in energy prices—expected to surge by 2.00% month-on-month in September. In contrast, food price inflation is expected to slow down, with a projected month-on-month increase of 0.19%, lower than August's 0.46%.

In specific categories, core goods prices are expected to continue to rise moderately. Although the growth rates of clothing, new cars, and used cars have slowed, other categories are expected to accelerate again after an unexpected decline in August. In terms of housing rent, August data was slightly above trend levels, and a pullback is expected in September, with a month-on-month growth rate below 0.30%. Core services inflation excluding housing is expected to rebound to 0.40%, mainly driven by medical services, while the growth of airfares and hotel prices has weakened.

Morgan Stanley also pointed out several key observations: first, while the speed of tariff transmission continues, it is becoming more gradual; the ISM and PMI price indicators, although still at high levels, have recently declined, reducing the likelihood of core goods month-on-month growth exceeding 0.4%; second, auto insurance inflation is expected to continue to slow, with rate filings indicating that its year-on-year increase may drop below 2% by the first quarter of 2026; third, the seasonal adjustment factor for used car CPI may be biased, potentially affecting policymakers' accurate interpretation of inflation data.

Additionally, Morgan Stanley expects the core Personal Consumption Expenditures (PCE) price index to rise by 0.30% month-on-month in September, slightly higher than the previous month's 0.23%. Among them, financial services inflation will remain at a high level of 0.53%, reflecting the strong performance of the stock market in July and August;Medical service inflation is expected to rise from 0.09% in August to 0.50%, with the core services PCE excluding housing projected to increase by 0.32% month-on-month