Wall Street may face the most turbulent earnings season in years!

S&P 500 component stock options data shows that investors expect the average price volatility after the earnings report release to reach 4.7%, close to the highest level since the earnings season began in 2022, set in July. Among them, AI and technology stocks are the focus of volatility, with individual stock skewness being flatter than the index, and traders are more inclined to chase the upward momentum of specific companies, especially AI-related stocks

Investors are once again preparing for significant market volatility during earnings season, as they are willing to pay high costs for speculation amid a market that has shown signs of fatigue after reaching historic highs.

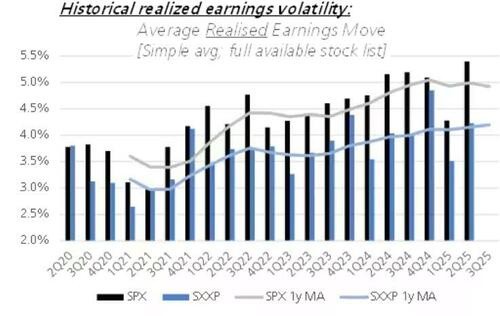

According to media reports on Monday, options data for S&P 500 constituents indicates that investors expect an average price volatility of 4.7% following earnings releases, close to the highest level since July when the earnings season began in 2022.

The sharp rise in option prices reflects the market's expectations for significant volatility in individual stocks, a surge in volatility expectations coinciding with multiple challenges facing the market, including heightened investor concerns over government shutdowns, the impact of trade policies on corporate profits, and the risks of an AI stock bubble.

Mandy Xu, head of derivatives market intelligence at the Chicago Board Options Exchange, stated:

At the individual stock level, significant volatility is being priced in. The market rally is primarily driven by AI and tech stocks, but the valuations and forward earnings prospects of these stocks are facing increasing scrutiny.

Citigroup strategists noted that, unlike the previous quarter, option prices have risen in anticipation of this volatility. Investors expect stock-specific factors to drive volatility in the near term, while the government shutdown means the market is in a vacuum of macro catalysts.

Options Market Reflects Record Volatility Expectations

According to data compiled by Bloomberg, the 4.7% average volatility implied by S&P 500 index options is comparable to levels seen in July, when the expected volatility reached the highest level since 2022, marked by JPMorgan's earnings release as the start of the earnings season.

UBS strategists indicated that actual stock price volatility following U.S. earnings last quarter peaked and has been on an upward trend since 2021, a trend also observed in European markets. Citigroup pointed out that stock correlations are extremely low, with both actual and implied volatility close to their lowest levels in at least a decade.

Vishal Vivek, a stock and derivatives trading strategist at Citigroup, believes:

The government shutdown means we are in a vacuum of macro catalysts, and at least from the perspective of individual stock options, positions have been tightened, setting up an interesting scenario for the latter half of October and early November.

AI and Tech Stocks Become the Focus of Volatility

Market observers have noted that individual stock skewness is flatter than that of the index, with traders more inclined to chase the gains of specific companies, particularly those related to AI. One factor supporting the slight increase in index volatility is low correlation; while individual stocks are more volatile than the S&P 500 index, they are moving in different directions, which helps keep index volatility moderate.

Cboe analyst Xu stated:

This earnings season will be crucial in determining whether the AI theme continues to dominate the market. The market rally is primarily driven by soaring AI and tech stocks, but there is increasing skepticism regarding the valuations and forward earnings prospects of these stocks.

This quarter, consumer discretionary, technology, and healthcare companies are expected to experience some of the largest volatility. According to data compiled by Bloomberg, the implied volatility for consumer discretionary stocks reached its highest level since 2020 at the start of the earnings season, while the materials sector, although lower, still recorded its highest level in three years

Market Repricing Reflects "Violent" Volatility

Alex Kosoglyadov, Managing Director of Global Equity Derivatives at Nomura Holdings, stated that the extreme volatility of large stocks such as Oracle Corporation and Advanced Micro Devices has led the options market to reprice other individual stocks.

"You see some large-cap stocks experiencing real violent fluctuations," he said. "This shows the power of the market; people really don't want to short volatility—you might encounter some kind of earnings surprise and huge price swings."

JP Morgan emphasized in August that investors looking to build discrete baskets may be focusing on post-earnings volatility to find bargains, as implied volatility often collapses, a phenomenon particularly evident after the last earnings season. Options traders have already pushed up the implied volatility of S&P 500 constituents, which may reflect bets on Mag7 stocks amid ongoing attention to AI and large tech stocks