$30 billion evaporated in a day! How the rare "bloodbath" in the history of American fintech came about

Fiserv's stock price plummeted 44% in one day, marking the largest decline since its listing nearly forty years ago. This crash appears to stem from the new CEO's withdrawal of previous performance guidance, but it actually exposes management failures: mispricing strategies, overpromising growth, and a corporate culture that is slow to respond to customer needs. The warning for investors is that even the most entrenched companies in the digital economy can collapse due to management mistakes

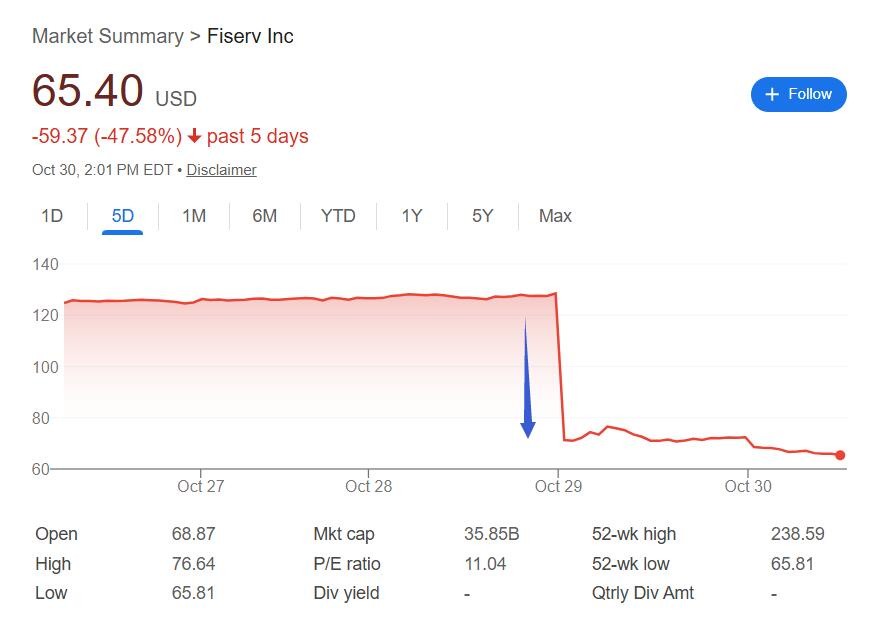

This Wednesday, the American fintech industry experienced one of the most shocking "bloodbaths" in recent years: fintech giant Fiserv's stock price plummeted by about 44%, marking the largest single-day drop in the company's nearly forty-year history, with a market value evaporating by approximately $30 billion.

On the surface, Fiserv's stock collapse was attributed to the new CEO Mike Lyons retracting previous performance guidance, but it actually exposed management failures: mispricing strategies, overpromising growth, and a corporate culture that is slow to respond to customer needs.

Lyons, who joined Fiserv in January and officially took over as CEO in May, announced during the earnings report on Wednesday that the full-year adjusted earnings per share (EPS) expectation was lowered from $10.15 to $10.30 to $8.50 to $8.60, a reduction of over 16%. Revenue growth expectations were cut by more than half, from 10% to 3.5%~4%.

Fiserv's third-quarter performance also fell far short of Wall Street expectations: revenue grew only about 1% year-on-year to $4.92 billion, over 8% lower than the expected $5.36 billion, and the adjusted EPS was $2.04, nearly 23% lower than the expected $2.64.

This crisis at Fiserv is not a technical failure but a concentrated manifestation of management negligence. Before leaving to serve in the Trump administration, former CEO Frank Bisignano set overly aggressive growth targets for the company, and the pricing strategy implemented on the flagship product Clover led to a massive loss of customers. This serves as a warning to investors: even the most entrenched companies in the digital economy can collapse due to management errors.

On Thursday, Fiserv's stock price further declined, with intraday losses expanding to nearly 7% during the midday session, exacerbating shareholder losses. As of Wednesday's close, the stock has fallen nearly 66% this year, potentially making it the worst-performing component of the S&P 500 index this year.

Customer Rebellion and Pricing Errors

Reports on Thursday indicated that Lyons quickly discovered he was facing a customer crisis after taking office. According to insiders, customers had repeatedly expressed dissatisfaction with the high fees associated with the Clover point-of-sale system, which they viewed as unnecessary burdens. An increasing number of merchants began to turn to cheaper alternatives like Square or Toast under Block, showing no willingness to return.

Clover was originally the core of Fiserv's growth strategy. Launched in 2010, this stylish payment terminal helped the company's predecessor, First Data, penetrate the small merchant market and continued to maintain growth momentum after being acquired by Fiserv in 2019. However, to ensure profits, Bisignano and his team began layering various "value-added service" fees on the product This strategy has boosted revenue in the short term, but at a high cost. William Blair analyst Andrew Jeffrey questioned in a report: "We doubt how many value-added services are truly robust software, and how many are just hollow charges. In a competitive market like merchant payment processing, innovation is key, and we believe Fiserv's ability to gain economic share has been impaired because the company has been focused on short-term performance at the expense of long-term competitive advantage."

Earlier this year, analysts had already noticed unusual signs: Clover's revenue growth was far outpacing the growth in payment volume processed, which should typically grow in sync. A collective lawsuit also alleged that Fiserv forcibly migrated up to 200,000 merchants using the old Payeezy system to Clover in 2023, attempting to boost Clover's revenue, but these customers subsequently flowed en masse to competitors.

Performance Collapse and Management Disorder

The earnings report released this Wednesday revealed more disturbing details. The company's Financial Solutions division—providing underlying technology for thousands of banks and credit unions across the U.S.—saw a 3% decline in revenue in the third quarter, with profit margins plummeting to 42.5%, down about 5 percentage points from the same period last year. This division also experienced a significant technical failure earlier this year.

Lyons admitted during Wednesday's earnings call: "This is not the reset I wanted or expected. There are a lot of embedded assumptions—assumptions far removed from the main projects—that are difficult to achieve even with good execution." He stated that the challenges currently faced are "largely self-inflicted."

After joining, Lyons ordered a thorough review of the company's finances, involving senior deputies from the merchant and banking divisions. The review revealed that many measures taken to achieve previous goals were "too short-term oriented," overly emphasizing cost-cutting to meet quarterly targets, which harmed the ability to deliver products to customers.

Former CEO Bisignano did not believe the targets he set were too high. Media reports indicated that insiders revealed he attributed the stock price plunge to Lyons' performance during his tenure. In February of this year, during one of his last conference calls before stepping down as Fiserv CEO and Chairman, Bisignano stated: "We are not pivoting, nor are we rethinking. We are going full speed ahead without hitting the brakes; that is our approach. We like it this way."

Wall Street's Harsh Judgment

Analysts quickly reacted to Fiserv's disastrous performance with ruthless criticism.

BTIG described Fiserv's earnings report as "shockingly bad" and "terrible." Analysts at William Blair wrote in their report: "Given that we believe the third-quarter revenue and earnings per share were shockingly poor, along with the sudden management transition, we can no longer recommend Fiserv."

Jefferies analyst Trevor Williams stated that Fiserv's guidance downgrade was "difficult to understand." Truist Financial analyst Matthew Coad remarked: "Frankly, we find it hard to recall any sub-industry we cover that has experienced such a level of performance shortfall and guidance downgrade." Mizuho analyst Dan Dolev remains cautiously optimistic, continuing to give the stock an outperform rating. He likens the situation to an emergency room: "It usually starts with a pain here or there, one thing leads to another, and then you see massive organ failure. I won't give up. If the patient survives organ failure, they can actually recover. The reset is painful, but it's not game over."

Fiserv announced a series of remedial measures, including reversing the pricing changes for Clover, launching a new technology strategy, and a major leadership overhaul.

Starting in December this year, Fiserv's Chief Operating Officer Takis Georgakopoulos will serve as co-president alongside former UnitedHealth Group Optum Financial Services CEO Dhivya Suryadevara. The company also appointed former Global Payments Chief Financial Officer Paul Todd as the new CFO and introduced three new board members, including former Royal Bank of Canada CEO Gordon Nixon as independent chairman.

For investors, this rare "bloodbath" in fintech history brings a profound lesson: in the current environment of intensified competition in the digital payments market and declining investor tolerance, even industry giants can face catastrophic consequences due to management missteps. The fact that Bisignano sold over $558 million worth of Fiserv stock between May and July—at an average price of about $170 per share, more than double Wednesday's closing price of $70.60—adds a touch of irony to this corporate crisis