Wall Street warns: The market is too optimistic about inflation, beware of the risk of "hawkish surprises"

Deutsche Bank and JP Morgan warned that investors may underestimate the persistence of inflation and the lagging effects of tariffs. Deutsche Bank believes that strong economic growth, rapid interest rate cuts, fiscal stimulus, and rising energy prices are accumulating inflationary pressures; JP Morgan estimates that tariffs could push the U.S. core CPI up to 4.6% by 2026. If inflation exceeds expectations, central banks may be forced to turn hawkish again, leading to a repeat of stock market corrections and gold rebounds

With the recent easing of international trade tensions, financial market concerns about inflation have significantly cooled, but the latest analyses from Deutsche Bank and JP Morgan warn that this optimism may be premature. Investors may be underestimating the multiple price pressures lurking in the economy, facing the risk of a "hawkish surprise" from central banks that is stronger than expected, which could impact the stock and bond markets.

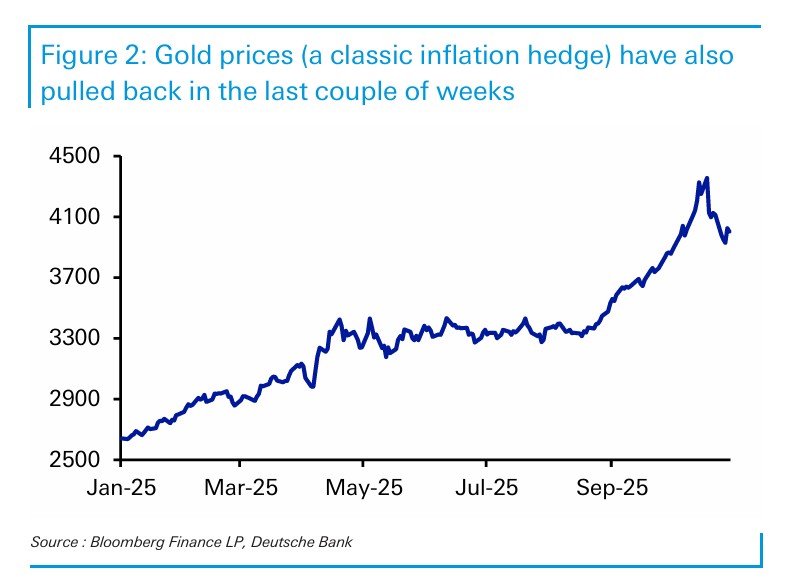

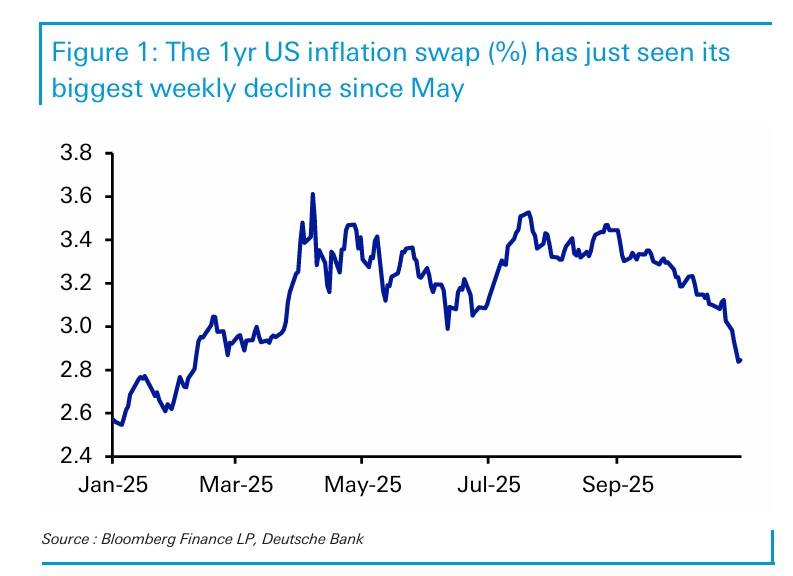

According to the Chase Trading Desk, Deutsche Bank noted in a report on November 3 that, benefiting from last week's trade easing, the 1-year inflation swap in the U.S. recorded its largest weekly decline since May. Meanwhile, the price of gold, a traditional inflation hedge, has also retreated from its highs.

However, central bank officials have been more cautious. The Federal Reserve released hawkish signals after last week's interest rate meeting, with Chairman Powell suggesting that another rate cut in December is not a certainty. This statement contrasts with the market's dovish expectations and adds uncertainty to the future policy path. JP Morgan also emphasized in a report on October 31 that the inflation impact from tariffs, although lagging, will eventually manifest and may be more persistent than expected.

If inflation proves more resilient than the market imagines, investors will face multiple risks. First, a hawkish shift from central banks that exceeds expectations may re-emerge, putting pressure on asset prices. Second, physical assets like gold, which perform well in inflationary environments, may regain favor. Finally, historical experience shows that a hawkish shift from central banks often accompanies stock market sell-offs, as seen in 2015-16, late 2018, and 2022.

Deutsche Bank: Six Factors That May Keep Inflation Above Expectations

Despite strong market optimism, Deutsche Bank believes there are several reasons to suggest that the market may once again underestimate inflation's stickiness, a situation that has repeatedly occurred in the post-pandemic cycle. The report lists six key factors:

- Significant Demand-Side Pressure: Recent global economic activity data has generally exceeded expectations. The Eurozone's October composite PMI preliminary value reached a two-year high, and U.S. PMI data has also shown resilience, with the Atlanta Fed's GDPNow model predicting an annualized growth rate of 3.9% for the third quarter. The strong stock market rally has also brought about a positive wealth effect.

- Lagging Effects of Monetary Easing: The Federal Reserve has cumulatively cut rates by 150 basis points since September 2024, while the European Central Bank is set to cut rates by 200 basis points from mid-2024 to mid-2025. The effects of monetary policy typically have a lag of over a year, meaning the impact of these easing measures will continue into 2026

- The impact of tariffs has not yet fully manifested: Although market turbulence peaked in April, many tariff measures did not take effect until August. These costs take months to fully transmit to the consumer end. There is still a possibility of additional tariffs in the future.

- European fiscal stimulus is on the way: Planned fiscal stimulus in Europe will further increase demand pressure, while the current unemployment rate in the Eurozone is near historical lows, and the idle capacity in the economy is far less than in the 2010s.

- Oil prices are rising again: The latest sanctions and OPEC+'s decision to pause production increases are driving oil prices higher once more.

- Inflation continues to exceed targets: Inflation rates in major economies remain above central bank targets. The U.S. CPI data for September was strong, with a 3-month annualized growth rate of core CPI reaching 3.6%. The latest core inflation rate in the Eurozone is 2.4%, above expectations, and has remained above 2% since the end of 2021. Japan's Tokyo CPI data for October also exceeded expectations, with the national inflation rate for September still at 2.9%, consistently above the Bank of Japan's target since early 2022.

Tariff transmission is delayed, but it will eventually arrive

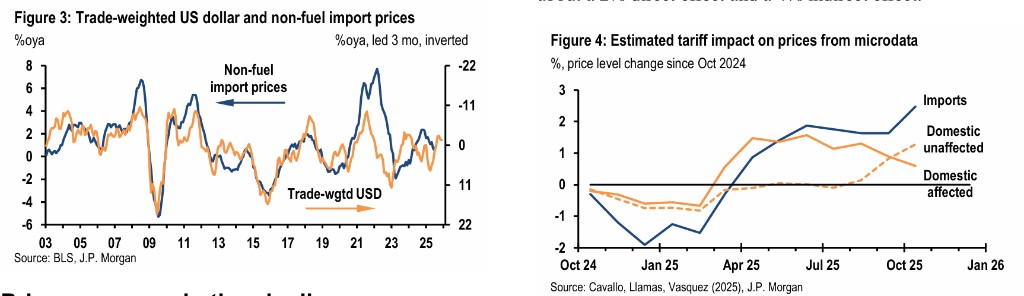

Among the many inflation-driving factors, the impact of tariffs is particularly noteworthy. JP Morgan's research report delves into this issue, suggesting that although the transmission process is slower than expected, U.S. consumers will ultimately bear most of the tariff costs.

According to JP Morgan's estimates, as of late October, this year's tariff revenue has exceeded last year's by more than $140 billion, with an annual increase expected to be around $200 billion. These costs were initially absorbed by U.S. companies by squeezing profit margins, but surveys indicate that companies plan to pass a larger proportion of these costs onto consumers.

The bank predicts that U.S. core CPI inflation may peak in the first quarter of 2026, reaching 4.6% (quarter-on-quarter annualized). Tariffs are expected to cumulatively push core CPI up by about 1.3 percentage points by mid-next year.

The delayed transmission of tariffs to consumer prices is due to several reasons: phased implementation of tariffs, importers delaying payments using bonded warehouses, the time it takes for production chains to transmit costs, and some companies using inventory to stabilize prices. However, companies cannot indefinitely absorb profit squeezes. Surveys from the New York Fed, Atlanta Fed, and Richmond Fed all show that companies plan to pass on 50% to 75% of tariff costs. JP Morgan warns that if companies lack pricing power and cannot pass on costs, the result will be cost control through reduced investment and layoffs, which will also significantly drag on economic activity.

"Hawkish surprises" could severely impact stocks and bonds, while physical assets like gold will regain support

If the market's judgment on inflation is incorrect, investors will face threefold risks.

First, more "hawkish surprises" from central banks. Deutsche Bank's report points out that the Fed's hawkish stance last week is an example. Looking back at this cycle, investors have repeatedly been surprised by premature expectations of interest rate cuts. The report also mentions that the Fed has implemented the fastest round of interest rate cuts since the 1980s in non-recession periods since September 2024, and further easing may be limited Secondly, higher-than-expected inflation will once again support physical assets such as gold. The report believes that the recent pullback in gold prices coincided with a decline in inflation concerns, and once inflation resilience exceeds expectations, this trend will be reversed. History shows that during inflationary periods, physical assets that can retain value often perform exceptionally well.

Finally, in addition to being a clear negative for bonds, the central bank's "hawkish turn" has historically often been accompanied by significant pullbacks in the stock market. The report cites data showing that the Federal Reserve's hawkish actions in 2015-2016 (first rate hike), late 2018 (continuous rate hikes), and 2022 (significant rate hikes) all coincided with notable sell-offs in the S&P 500 index. Historically, interest rate hikes are one of the most common factors leading to significant pullbacks in U.S. stocks.