Ray Dalio: The end of QT by the Federal Reserve = Stimulating the economy in a bubble, the United States' "big debt cycle" has entered the most dangerous stage!

Powell stated that "reserves will be increased again at the appropriate time." In Dalio's view, this means that QE is returning, but the current environment (with significant market bubbles) is vastly different from the past (during economic recessions). Due to highly stimulative fiscal policies—massive debt stock and deficits financed through large-scale government bond issuance—QE is essentially monetizing government debt rather than merely providing liquidity to the private sector, which could lead to a replay of the liquidity frenzy seen on the eve of the 1999 bubble burst

Ray Dalio, the founder of Bridgewater Associates, issued a warning that the Federal Reserve's decision to end quantitative tightening (QT) may be adding water to a bubble, creating a larger bubble.

On Wednesday local time, Dalio published an article on LinkedIn pointing out that the current loose monetary policy of the Federal Reserve is being implemented at a time when asset valuations are high and the economy is relatively strong, and ending QT is "stimulus into a bubble" rather than the traditional "stimulus into a depression."

Federal Reserve Chairman Jerome Powell recently stated that as the banking system and the economy expand, the Fed "will increase reserves again at the appropriate time." In Dalio's view, this means that QE is returning—only packaged as a "technical operation."

Dalio believes that the United States' "big debt cycle" has entered its most dangerous phase, and the market should not ignore this fact:

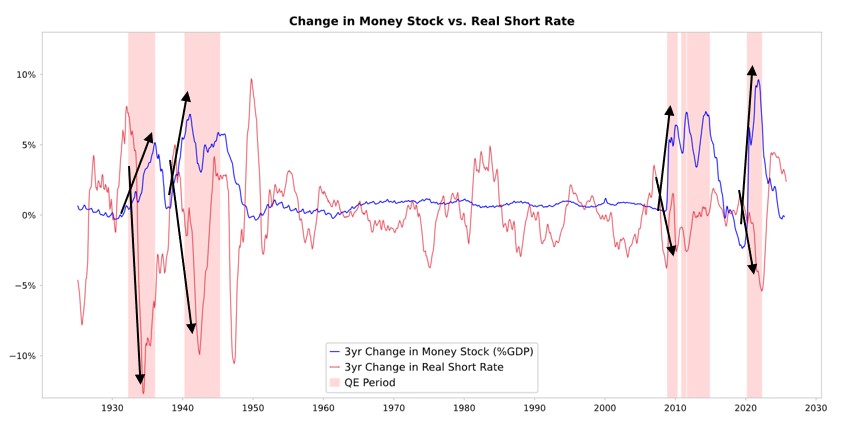

When the supply of U.S. Treasuries exceeds demand, the Federal Reserve "prints money" to buy bonds, while the Treasury shortens the duration of bond sales to fill the gap in long-term bond demand, these are all typical late-stage dynamics of the "big debt cycle."

Dalio expects that in a liquidity-rich environment, long-duration assets (such as technology and AI stocks) and inflation-hedging assets (such as gold) will benefit, but this "liquidity bubble" will ultimately face the challenges of risk accumulation and policy tightening.

QE Transmission Mechanism: Relative Prices Drive Market Flows

Dalio explained the market transmission mechanism of quantitative easing in detail. He pointed out that all financial flows and market fluctuations are driven by relative attractiveness rather than absolute attractiveness. Investors make choices based on the relative expected total returns of different assets, where expected total return equals asset yield plus price changes.

Taking the current market as an example, the yield on gold is 0%, while the yield on 10-year U.S. Treasuries is about 4%. If the expected annual price increase of gold is less than 4%, investors will prefer bonds; conversely, they will prefer gold. Considering inflation factors, an increase in money and credit supply by the central bank will raise inflation expectations, thereby enhancing the relative attractiveness of gold compared to bonds.

The implementation of QE typically creates liquidity and lowers real interest rates. If liquidity primarily flows into financial assets, it will push up asset prices, lower real yields, expand valuation multiples, compress risk spreads, and elevate gold prices, forming "financial asset inflation." This effect will widen the wealth gap between asset holders and non-holders.

Unprecedented "Stimulus in a Bubble"

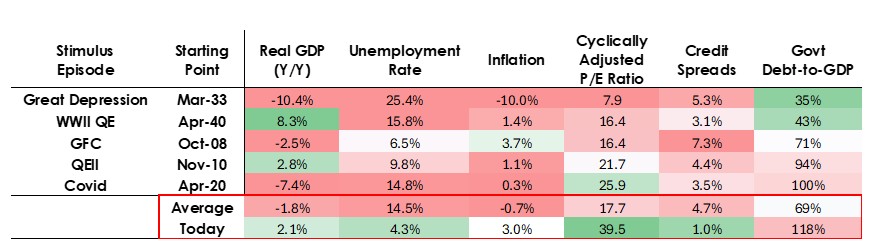

Dalio emphasized that the current environment in which the Federal Reserve is implementing QE is fundamentally different from the past, significantly increasing policy risks. Historically, QE has typically been deployed during economic recessions or extreme weakness, characterized by the following: asset valuations falling and being reasonable, economic contraction, low inflation, severe debt and liquidity issues, and wide credit spreads However, the current situation is completely the opposite. Asset valuations are at high levels and continue to rise, with the S&P 500 earnings yield at 4.4%, while the nominal yield on 10-year U.S. Treasuries is 4%, and the real yield is about 1.8%, with the equity risk premium at only about 0.3%. The economy is relatively strong, with an average real growth rate of 2% over the past year and an unemployment rate of only 4.3%.

The inflation rate is slightly above the target level at about 3%, with de-globalization and tariff costs putting upward pressure on prices. Credit and liquidity are abundant, with credit spreads close to historical lows. Implementing QE in this environment constitutes "stimulus into a bubble."

Government Debt Monetization, Replaying the Liquidity Frenzy Before the 1999 Crisis?

Dalio believes that due to highly stimulative fiscal policy—massive debt stock and deficits financed through large-scale issuance of government bonds, QE is actually monetizing government debt rather than simply providing liquidity to the private sector.

If the (Federal Reserve's) balance sheet begins to expand significantly while interest rates are lowered and the fiscal deficit remains large, we would view this as a typical monetary and fiscal interaction between the Federal Reserve and the Treasury aimed at monetizing government debt.

This makes the current policy "look more dangerous and more inflationary."

Dalio warns that in the short term, the market may experience a "liquidity melt-up" similar to the period before the bursting of the 1999 internet bubble or during the QE period of 2010-2011.

In Dalio's view, the current U.S. policy mix—expanding fiscal deficits, restarting monetary easing, deregulation, and AI prosperity—is forming a "super loose situation betting on growth."

While such policies often create asset booms in the short term, they also tend to mean: bubbles inflate faster; inflation becomes harder to control; risks accumulate deeper. And when policies are forced to reverse, the costs will be greater.

He expects QE to push down real interest rates, increase liquidity by compressing risk premiums, and elevate price-to-earnings multiples, particularly benefiting long-duration assets (technology, AI, growth stocks) and inflation-hedging assets like gold. Once inflation risks awaken again, tangible asset companies such as mining and infrastructure may outperform pure long-duration tech stocks