Next week's focus: "NVIDIA earnings report," Morgan Stanley: It will be the strongest in the past few quarters, breaking the perception of "growth peaking."

Morgan Stanley stated that industry research shows a substantial acceleration in demand, and NVIDIA has completely resolved early rack-related issues, while demand continues to surge. The full-scale ramp-up of Blackwell chips will be a key driving factor. NVIDIA's positive statements at the GTC conference further reinforced this trend. Currently, growth bottlenecks are more apparent on NVIDIA's supply side as well as in supporting hardware (storage, servers) and space/power aspects, but these should not dampen the significant trend of accelerating demand

Morgan Stanley raised the target price for NVIDIA to $220. Analysts expect that NVIDIA's upcoming third-quarter financial report will be a breakthrough quarter, likely dispelling market perceptions of its growth peaking.

According to news from the Wind Trading Desk, Morgan Stanley analyst Joseph Moore stated in a report on November 14 that industry research shows a substantial acceleration in demand, and NVIDIA has fully resolved early rack-related issues, while demand continues to surge. Currently, growth bottlenecks are more apparent on NVIDIA's supply side and in supporting hardware (storage, servers) and space/power aspects, but these should not hinder the clear trend of accelerating demand.

The ramp-up phase of Blackwell chips entering full-scale production will be a key driving factor. NVIDIA's positive statements at the GTC conference further reinforced this trend.

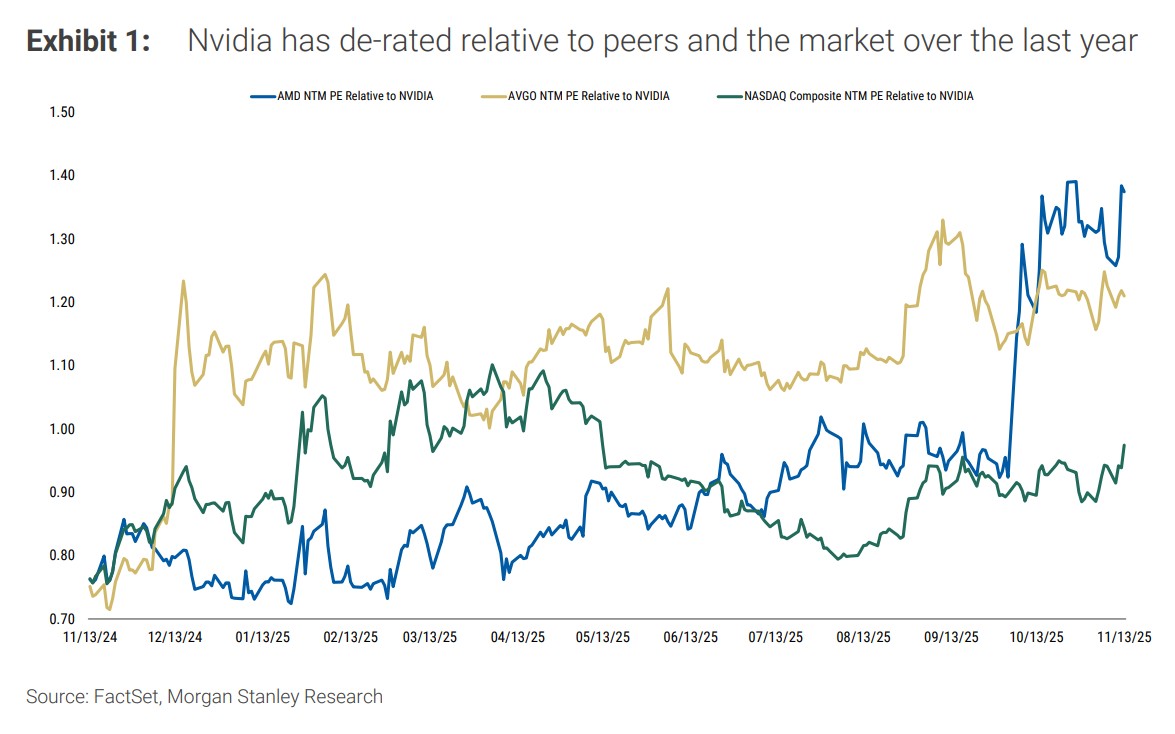

Morgan Stanley believes that next week's earnings will be NVIDIA's strongest financial report in several quarters. Although NVIDIA's stock performance has been solid, it has lagged behind its AI peers, and this situation is expected to reverse.

Supply and demand data shows demand acceleration exceeds expectations

Morgan Stanley's industry research indicates that demand signals from NVIDIA's customers and suppliers in the third quarter point to accelerated growth, contrasting sharply with the market's general expectation that NVIDIA's growth metrics have peaked.

On the customer side, third-quarter capital expenditure expectations for cloud services have been raised to $142 billion, with the four major hyperscale cloud service providers each increasing by over $20 billion. Compared to the dollar growth in 2025, the current increase has reached $115 billion, which is $60 billion higher than a quarter ago.

From the supplier perspective, ODM manufacturer Quanta expects its AI server revenue to accelerate growth in the first quarter of 2026, with a year-on-year increase of over 100%. To support this demand, Quanta plans to double its AI server production capacity next year, as order visibility has extended to 2027.

Blackwell chips become the core growth engine

Morgan Stanley raised NVIDIA's revenue expectations for October from $54.4 billion to $55 billion, and for January from $61.2 billion to $63.1 billion. Analysts pointed out that achieving $8 billion in quarter-on-quarter growth in both October and January would set a historical record for the industry.

Blackwell chips remain the preferred choice for AI chips, with very strong demand signals for Vera Rubin. Although competitors are showing enthusiasm, this reflects the progress and the strength of market demand.

NVIDIA CEO Jensen Huang previously stated that revenue over the next five quarters needs to be increased within the range of $70 billion to $80 billion (Morgan Stanley raised it by $22 billion), while the current stock price is 10% lower than the peak following Huang's statement

Morgan Stanley raised its fiscal year 2027 expectations for NVIDIA from revenue of $278 billion/non-GAAP earnings per share of $6.59 to $298.5 billion/$7.11. Analysts believe that considering the strong order backlog, the company may provide higher guidance, which mainly depends on how conservative it can remain in a strong demand environment.

The new target price of $220 is based on a 26 times price-to-earnings ratio of the ModelWare earnings per share expectation of $8.43 for fiscal year 2027, which is approximately equivalent to a 25 times non-GAAP price-to-earnings ratio. This valuation reflects a discount compared to the average forward price-to-earnings ratio (32 times) and two-year price-to-earnings ratio (28 times) over the past two years, reflecting expectations of slowing growth, while also being at a discount compared to larger AI semiconductor peer Broadcom