The Federal Reserve's restart of "quantitative easing" is not far off, with an announcement as early as December?

Key indicators measuring the cost of short-term borrowing continue to send warning signals. The tri-party repurchase rate rose again this week. After Federal Reserve officials released strong signals for "balance sheet expansion," Citigroup predicts that the Federal Reserve may announce a new round of Treasury purchases as early as December, to be implemented in January, to alleviate pressure in the funding markets. This shift indicates that years of quantitative tightening (QT) are coming to an end

After Federal Reserve officials released strong signals indicating that the central bank is "not far" from restarting balance sheet expansion, Citigroup predicts that the Fed may announce a new round of Treasury purchases as early as December and implement it in January.

Federal Reserve Officials Release Clear Signals

John Williams, President of the New York Fed, spoke this week, suggesting that the Fed will soon begin to expand its balance sheet to alleviate pressure in the funding markets.

Williams stated:

Based on recent ongoing pressures in the repo market and other signs that reserves have shifted from abundant to adequate, I expect that we are not far from reaching adequate reserve levels.

The New York Fed held an unscheduled meeting with major Wall Street banks this week, the core agenda of the meeting was to solicit feedback from primary dealers (i.e., banks that underwrite government debt) on the usage of the Fed's standing repo facility. This highlights officials' concerns about the tightness in the U.S. money markets.

Key indicators measuring short-term borrowing costs continue to send warning signals. The tri-party repo rate rose again this week, at one point exceeding the Fed's reserve balance rate by nearly 0.1 percentage points.

Roberto Perli, head of market operations at the New York Fed, acknowledged that some borrowers have been struggling to obtain repo funding close to the central bank's reserve rate, with the share of repo transactions conducted at rates above the reserve balance rate reaching the highest levels since the end of 2018 and 2019.

Analysts warn that as the year-end approaches, the market will face more pressure. Banks typically reduce their balance sheet size at year-end for financial reporting purposes, which could exacerbate cash tightness. After three years of quantitative tightening, excess cash in the banking system has significantly decreased.

Balance Sheet Reduction Will Stop in December, Bond Purchases May Start in January or February

Citigroup currently expects the Fed's balance sheet reduction to stop on December 1. The most likely path is for the Fed to announce more Treasury purchases at the January meeting, starting implementation on February 1.

However, the probability of announcing bond purchases at the December meeting is comparable to that in January. Since the end of October, pressures in the repo market have eased, with the secured overnight financing rate (SOFR) not exceeding 4% (the upper limit of the federal funds target range) in recent days. However, pressures may rise again in the coming weeks, increasing the urgency for a December announcement.

Citigroup also predicts that the Fed is most likely to lower the interest on reserve balances (IORB) by 5 basis points at the December meeting, which would help keep repo rates within the federal funds target range.

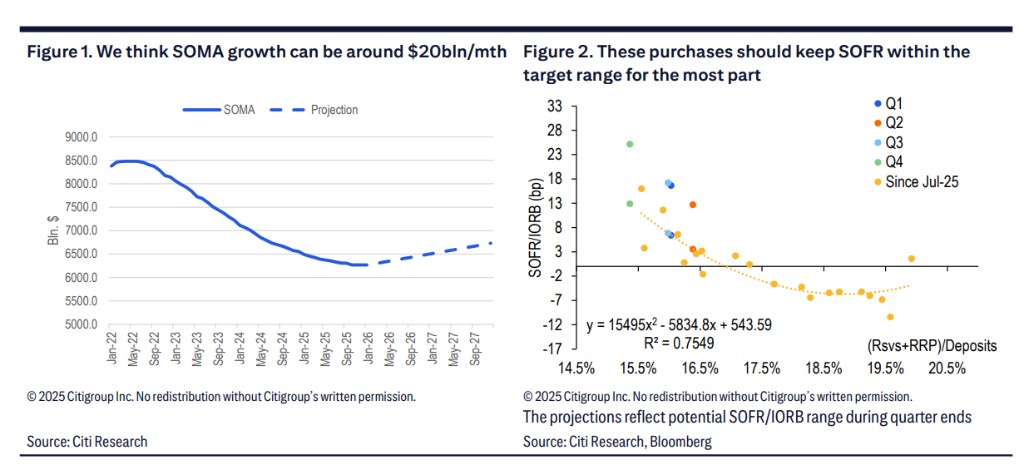

Monthly Net Purchases of $20 Billion Needed to Maintain Liquidity

Analysts believe that the Fed only needs to conduct relatively modest net purchases of Treasuries to maintain reserves in the adequate range.

With current reserve levels growing by about 5% annually (to keep reserves as a percentage of nominal GDP roughly unchanged), plus currency in circulation growing by about 5% annually, this means that SOMA needs a net increase of about $20 billion per month

In practical terms, this means that the Federal Reserve will reinvest all maturing Treasury bonds and additionally purchase about $20 billion in Treasury bonds to offset the asset reduction caused by the maturity of mortgage-backed securities (MBS). Citigroup believes that this scale of purchases is sufficient to keep the SOFR (as well as the Treasury General Collateral Rate, TGCR) within the target range on normal trading days next year.

Balance Sheet Size Forecast: Reaching $7 Trillion by the End of 2027

Citigroup estimates that the total assets of the Federal Reserve's balance sheet will steadily grow from $6.628 trillion in November 2025 to $7.068 trillion by December 2027.

Among these, the holdings of U.S. Treasury bonds will increase from the current $4.192 trillion to $5.022 trillion, while MBS holdings will gradually decline from $2.067 trillion to $1.682 trillion.

On the liability side, the reserve balance is expected to fluctuate upwards from the current $2.887 trillion, reaching $3.350 trillion by the end of 2027. The circulating currency will steadily grow from $2.423 trillion to $2.548 trillion. Notably, the balance of reverse repurchase agreements (RRP) is expected to remain at very low levels.

This growth path of the balance sheet reflects the Federal Reserve's shift from quantitative tightening to an "organic growth" model. However, Citigroup emphasizes that this does not represent a change in monetary policy stance, but rather a technical adjustment to accommodate the growth in the Federal Reserve's liability needs.