Huazhu Club FY25Q2 Minutes: Hanting 4.0 Signing Strong

$HWORLD-S(01179.HK) $H World(HTHT.US) The following are the minutes of Huazhu's Q2 2025 earnings call. For financial report interpretation, please refer to "Huazhu: Strengthening Fundamentals, Is Huazhu Ready to 'Squat and Jump'? -"

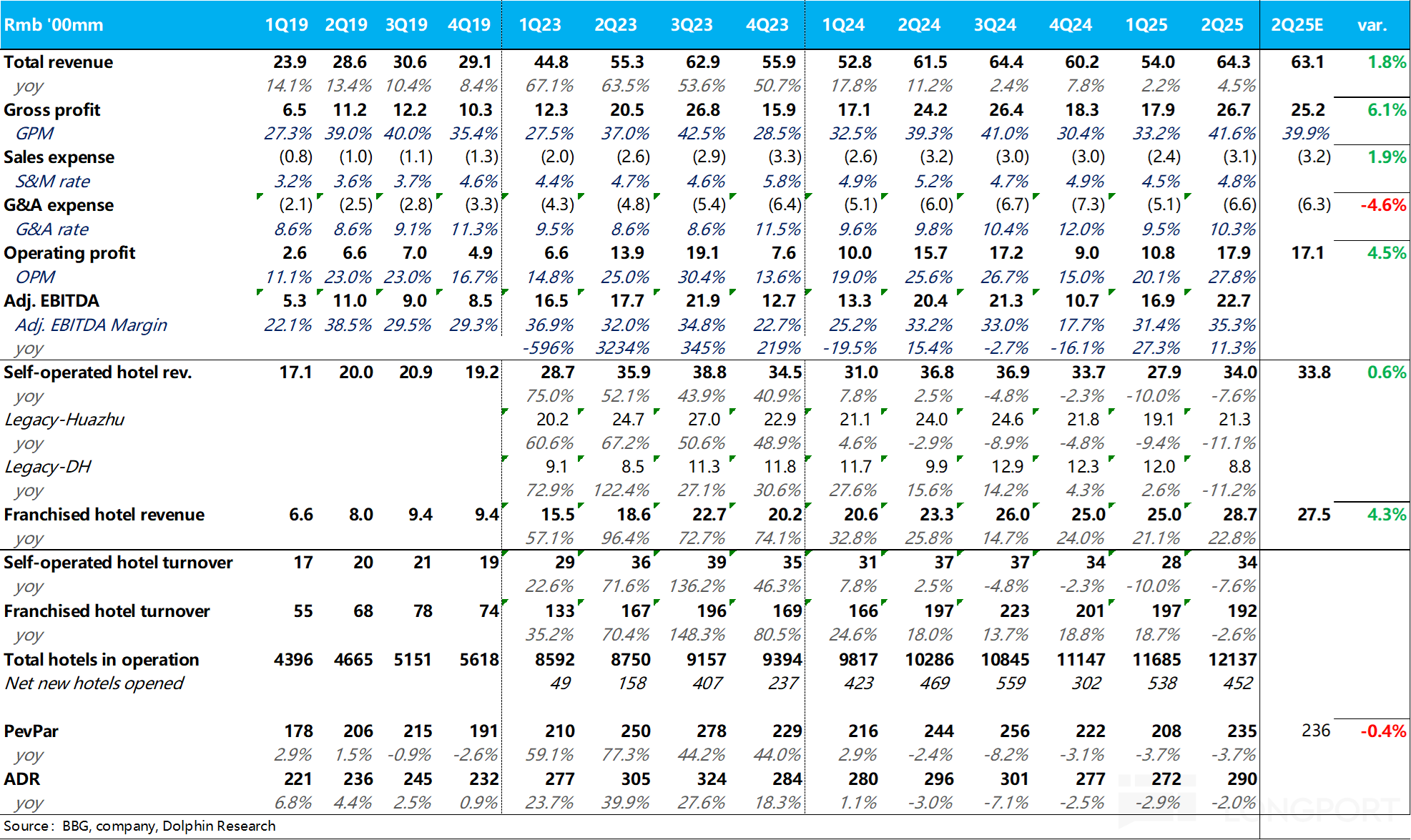

I. Review of Core Financial Information:

(1) Business Performance

- Operational Data: The number of rooms in operation increased by 18.3% year-on-year, with the group's GMV up 15% year-on-year to RMB 26.9 billion; H Rewards members reached 290 million (up 17.5% year-on-year), with member room nights exceeding 60 million (up 28.8% year-on-year).

- Brand Upgrade: The Hanting 4.0 version was officially released, bringing systemic reforms to the supply chain (lower CapEx/OpEx, higher quality, faster construction cycle); Orange Hotels surpassed 1,000 locations, becoming the second growth engine in the mid-range market; mid-to-high-end brands (such as Intercity) have over 1,500 hotels in operation and reserve (up 23.3% year-on-year).

- Asset-light Transformation: Revenue from management franchise and franchising business was RMB 2.9 billion (up 22.8% year-on-year), with a gross profit of RMB 1.9 billion (up 23.2% year-on-year), contributing 64% of the group's total gross profit.

(2) Performance Guidance

- Q3 group revenue is expected to increase by 2% to 6% year-on-year (excluding DH business, it is +4% to +8%);

- Q3 management franchise and franchising revenue is expected to increase by 20% to 24% year-on-year.

II. Detailed Content of the Earnings Call

2.1, Key Information from Executive Statements:

1. Industry and Positioning: Domestic travel numbers continue to grow, but hotel supply has increased rapidly over the past two years, combined with macroeconomic pressures on business and consumer spending, the industry remains under pressure. The group remains focused on the economy and mid-range segments to meet the public's demand for "high cost-effectiveness," strengthening long-term competitiveness.

2. Brand Upgrade and Product Optimization: Hanting ranks first among the top 50 global hotel brands and has launched version 4.0, achieving lower costs, higher quality, and higher efficiency through supply chain optimization, with the construction cycle shortened by about 30 days; Orange Hotels surpassed 1,000 locations, becoming the second growth engine in the mid-range market; Intercity is growing rapidly in the mid-to-high-end market, with RevPAR achieving positive growth.

3. Supply Chain Capability: By expanding the supplier pool, strengthening modular applications, and optimizing design, product quality is improved, CapEx/OpEx is reduced, and the construction cycle is shortened (e.g., the average construction cycle of Hanting 4.0 is shortened by 30 days), supporting high-quality development.

4. Membership and Direct Sales: H Rewards members are nearly 290 million, with CRS direct sales accounting for 65.1% (up 5.2 percentage points year-on-year); a price guarantee feature was launched, expanding the use of points and cross-industry cooperation to enhance stickiness and direct sales capability.

5. Asset-light Transformation and Financial Optimization: Management franchise and franchising business contributed 64% of the group's total gross profit (up 7.5 percentage points year-on-year); rental and owned business revenue and gross profit decreased by 7.6% and 13.4% year-on-year, respectively. The group improved profitability through rent renegotiations (rent reduction of RMB 390 million in the first half), revenue management, and cost optimization; dividends were declared and buybacks were maintained to ensure shareholder returns.

2.2, Q&A Analyst Questions and Answers

Q: What are the expectations for RevPAR in Q3 and 2025? Is there any change in the full-year revenue guidance? Will new hotels cause RevPAR cannibalization of old hotels? If so, does management have measures to mitigate this?

A: During the summer, we observed many local governments promoting tourism, such as offering ticket discounts and even free tickets to stimulate leisure travel demand. However, some areas were affected by extreme weather and macroeconomic uncertainties, resulting in overall summer performance slightly below previous expectations. Therefore, we expect a slight year-on-year decline in Q3 RevPAR, but the sequential decline will narrow significantly. Full-year RevPAR is expected to be slightly below previous guidance, but we will strive to achieve the original revenue targets. As for the impact of new hotels on old hotels, it does exist, especially in first- and second-tier cities, where older versions of hotels (such as Hanting 2.0/2.5) are less competitive. We are continuously launching new products, such as Hanting 4.0, Orange 3.0, and All Seasons 5.0, with significant improvements in product quality, which helps alleviate the pressure on old hotels. At the same time, first- and second-tier cities have more high-quality properties available for new openings, which will impact old hotels in the short term, but this is a necessary process. Our goal is not only to increase market share but also to enhance market share with high-quality products. Therefore, we are upgrading old hotels while being more rational in site selection for new openings.

Q: What is the rationale behind splitting gross profit into asset-light and asset-heavy businesses? Does this represent a strategic focus? Additionally, with a 20% decline in rental and owned business gross profit, what are the future improvement measures?

A: In recent years, we have actively promoted asset-light transformation, with rapid growth in management franchise and franchising business, becoming the main profit driver. Therefore, starting this quarter, we disclose the split of asset-light and asset-heavy to better reflect future strategy. The decline in rental and owned business gross profit is mainly due to continued scale reduction, resulting in declines in revenue, gross profit, and profit margin. However, we have taken several measures to improve: first, actively negotiating with landlords, with RMB 390 million in rent reduction agreements signed in the first half; second, strengthening revenue management, sales and marketing, and cost optimization. Even with the gradual reduction of rental business, we will strive to improve the performance of existing properties.

Q: We have seen a slowdown in new signings. How is the sentiment of franchisees under the current macroeconomic background? Will the full-year store opening plan be adjusted? Additionally, is there room for further optimization of the group's profit margin?

A: We have always adhered to the "high-quality growth" strategy rather than simply pursuing scale expansion, so we are more stringent in the selection of new properties and locations to ensure franchisee profitability and product quality. In terms of profit margin, benefiting from the increased contribution of asset-light, supply chain cost reduction, increased CRS direct sales proportion, and some rent reductions, the group achieved an adjusted EBITDA increase of 11.3% year-on-year despite the decline in RevPAR. Excluding share-based compensation expenses, SG&A decreased by about 1% year-on-year in the second quarter. We will still have some investments in the future, but they must consider reasonable ROI. In the long term, as the contribution of asset-light further increases, profit margins are expected to remain stable or gradually improve.

Q: How long will it take to alleviate the RevPAR pressure on old Hanting stores? Additionally, what is the long-term growth potential of Orange and Intercity in the mid-to-high-end market?

A: The Hanting brand has been upgraded to version 4.0, which is at the forefront in terms of design, quality, and efficiency. However, we have indeed observed that Hanting 2.0/2.5 and below versions face the greatest pressure. It is expected to take 1-2 years to resolve this issue through replacement or upgrade. This year, Hanting's new signings are very strong, and we will continue to open new stores while replacing or upgrading old stores to enhance competitiveness. As for Orange, the 3.0 version has been well received by franchisees and consumers, with the number of hotels exceeding 1,000. We hope it can become the second largest mid-range brand after All Seasons, with both occupying the first and second positions in the mid-range market. Intercity has developed rapidly in recent quarters with high quality and precise positioning, achieving positive same-store RevPAR growth in the second quarter, which is something few brands can achieve. In the next 3-5 years, we hope it will become a leading brand in the mid-to-high-end market. The current weak real estate market, with a large number of Grade A office buildings entering the market in first- and second-tier cities, provides an opportunity for us to create high-quality hotel products. Intercity will become the new standard for mid-to-high-end hotels.

Q: Can you provide more details on supply chain capability building and cost reduction effectiveness? Additionally, what is the pace of DH business transitioning to an asset-light model?

A: Since 2024, we have comprehensively upgraded supply chain capabilities: introducing more top suppliers, strengthening modular applications, and optimizing design and quality standards. For example, the cost of furniture and materials has decreased by about 10%-20% year-on-year; Hanting 4.0, due to modular applications, has shortened the construction cycle by about 30 days. The enhancement of supply chain capabilities helps us achieve higher efficiency and cost leadership. Regarding the DH business, there are many legal restrictions on lease contracts in Europe, especially in Germany, making them difficult to terminate. We are actively negotiating with landlords and continuously evaluating the profitability of inefficient hotels, with some lease adjustments underway. Future new contracts will be very cautious, aiming to gradually transition DH to an asset-light model.

<End Here>

Risk Disclosure and Statement of This Article:Dolphin Research Disclaimer and General Disclosure