Qualcomm (Minutes): Details and performance metrics of AI chips will be announced early next year.

The following are the minutes of Qualcomm's Q4 FY2025 earnings call organized by Dolphin Research. For an interpretation of the earnings report, please refer to Qualcomm: Shedding the 'Mobile Stock' Label, Is AI Computing Power the 'New Hope'?

I. $Qualcomm(QCOM.US) Key Financial Highlights

1. Cash Flow and Shareholder Returns: Generated a record $12.8 billion in free cash flow, returning nearly 100% to shareholders through buybacks and dividends.

2. Q1 FY26 Guidance:

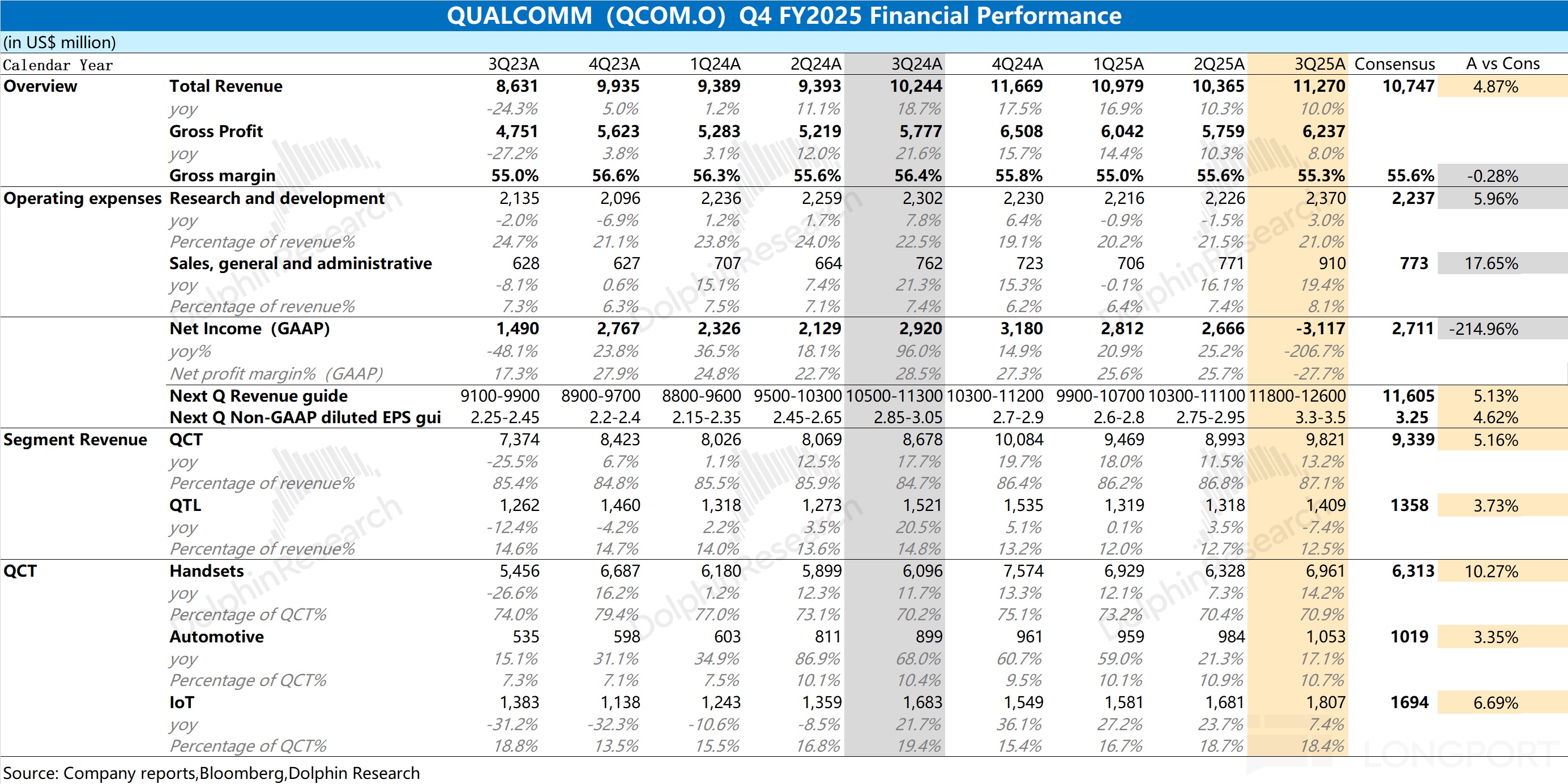

a. Revenue is expected to be between $11.8 billion and $12.6 billion, with EPS between $3.30 and $3.50.

b. QTL Business: Revenue is expected to be $1.4 billion to $1.6 billion, with an EBT margin of 74% to 78%.

c. QCT Business: Revenue is expected to reach a record $10.3 billion to $10.9 billion, with an EBT margin of 30% to 32%.

- Mobile Business: Expected to achieve 'low double-digit' growth (11-14%) quarter-over-quarter, driven mainly by the launch of new Android flagships.

- Automotive Business: Expected to be flat or slightly up quarter-over-quarter.

- IoT Business: Expected to decline quarter-over-quarter due to seasonal factors, consistent with last year's trend.

d. Tax Rate: The new tax law is expected to keep the future non-GAAP tax rate at 13%-14% and reduce cash tax expenses.

3. Long-term Goals: The company is steadily advancing towards the long-term revenue targets set on Investor Day, particularly the $22 billion target for automotive and IoT.

a. Automotive Business (Target $8 billion): Confident in achieving the target with the accelerated adoption of the Snapdragon Digital Chassis and 36% annual growth.

b. IoT Business (Target $14 billion): The growing importance of AI and low-power computing, along with 22% annual growth, also inspires confidence.

4. Progress in Growth Areas:

a. PC Sector: The launch of the Snapdragon X2 Elite/Extreme platform has expanded its technological leadership, with about 150 design wins, optimistic about the growth potential of AI PCs.

b. XR: Strong demand for AI smart glasses, exceeding expectations. The company remains the preferred platform for leading global manufacturers.

c. Industrial IoT: Unlocking access to 30 million users through customer interactions, project growth, and recent acquisitions, laying the foundation for strong future growth.

d. Automotive Sector: Has become the 'most strategic chip partner' for global automakers, accelerating the adoption of the Snapdragon Digital Chassis.

e. Networking Sector: Continued innovation and leadership in Wi-Fi, 5G, and edge AI will drive global content growth and application proliferation.

f. Emerging Opportunities: In addition to established targets, the company is actively seeking incremental opportunities in data centers and robotics.

II. Detailed Content of Qualcomm's Earnings Call

2.1 Key Information from Executive Statements

1. Overall Financial Performance: Fourth-quarter revenue of $11.3 billion, non-GAAP EPS of $3, both exceeding the upper end of expectations. FY2025 total revenue of $44 billion, up 13% year-over-year.

QCT Business: Fourth-quarter revenue of $9.8 billion, up 9% quarter-over-quarter. Full-year revenue reached a record $38.4 billion, up 16% year-over-year.

- Non-Apple business growth was particularly strong, up 18% year-over-year, exceeding expectations.

- Automotive Business: Fourth-quarter revenue exceeded $1 billion for the first time, with full-year revenue up 36%.

- IoT Business: Full-year revenue up 22%.

2. Business Unit Highlights:

a. Smartphones: Launched the next-generation flagship platform Snapdragon 8 Elite Gen 5, featuring the self-developed third-generation Oryon CPU, continuing to lead the market in performance. The Snapdragon Summit had a significant impact, with close cooperation with leading Chinese manufacturers such as Xiaomi, Honor, and vivo, and a solid ecosystem. Brand value has significantly increased, with Qualcomm and Snapdragon appearing on Interbrand and Kantar's global top brand lists for the first time.

b. AI PC: Launched the Snapdragon X2 Elite and X2 Elite Extreme platforms for high-end laptops. Surpassing Intel and AMD in speed and energy efficiency, NPU performance has once again set the industry benchmark. Approximately 150 AI PC designs using the Snapdragon platform are expected to hit the market by 2026, with strong momentum.

c. IoT and XR: Smart glasses are seen as personal AI devices connecting users, with the market reaching a turning point. Deep cooperation with Meta, providing Snapdragon platform support for its new smart glasses (such as Ray-Ban Gen 2). Collaborated with Samsung to launch the Galaxy XR headset and became the first device for Google's new AI-native operating system Android XR. Through acquisitions of companies like Arduino, integrated a vast developer ecosystem, accelerating the construction of a comprehensive edge AI development platform.

d. Automotive Business: Collaborated with BMW to launch the first L2+ level autonomous driving full-system solution Snapdragon Ride Pilot, debuting on the BMW iX3. Expanded cooperation with Google, integrating the Google Gemini model into the Snapdragon Digital Chassis to jointly create an in-car AI assistant.

e. Data Center Business: Officially announced entry into the AI data center inference market, launching AI 200 and AI 250 SoCs and related accelerator cards. Secured the first customer Humain, with deployment planned from 2026. Plans to announce a detailed roadmap for the data center business in the first half of 2026.

3. Future Outlook: The core of the strategy is to become a leader in extending AI capabilities from the cloud to edge devices such as phones, PCs, cars, and IoT. Promoting a hybrid AI model that enables 'edge + cloud' collaboration. Will continue to make progress in advanced robotics, next-generation ADAS, industrial edge AI, and 6G.

2.2 Q&A Session

Q: First, can you talk about what you see as Qualcomm's core competitive advantage in the data center field? Secondly, beyond what was disclosed in the press release, can you provide more details on the specifications of the AI 200 and AI 250 chips? Lastly, last quarter you mentioned cooperation with a 'hyperscale' customer, is this different from the cooperation announced with Humain? If so, is there any update on the timeline for that hyperscale customer cooperation?

A: We are very excited about entering the data center field and see it as a 'new chapter' in the company's diversified expansion. Our core competitive advantage lies in energy efficiency, generating the most tokens with the least power consumption. We are approaching this from two aspects: First, we have a highly competitive high-efficiency CPU that can be used for AI cluster head nodes and general computing; Second, we are building a new architecture specifically designed for AI inference. Our AI 200 and AI 250 chips and accelerator card solutions were developed under this strategy, and progress is satisfactory, with more details and performance metrics to be announced early next year.

Regarding customer cooperation, we have indeed had discussions with a 'hyperscale' customer and are very satisfied with the results. More details of this cooperation will be updated as part of our future data center roadmap release. The market clearly needs competition, and we will prove ourselves with Qualcomm's consistent product performance.

Q: Recently, there have been many rumors in the market about your largest Android customer (referring to Samsung) possibly planning to use more of its self-developed baseband chips. Can you talk about the visibility of business with that customer? And what changes do you expect in your share with that customer over the next year or so?

A: First, the high-end Android smartphone market is continuously expanding, bringing healthy growth to our Snapdragon platform. Even in a stable overall phone market, our Android business can continue to grow by increasing content and average selling price (ASP), mainly due to the expansion of the high-end market. Secondly, regarding our relationship with Samsung, we have long clarified that the new cooperation baseline is a 75% share, which is also our future financial forecast assumption. Although sometimes due to excellent execution, we achieve a higher share (such as 100% on the Galaxy S25), our planning and assumptions for future new models (such as the Galaxy S26) will always be based on this 75% share.

Q: We hear that the current mainstream AI training clusters have an installation cost of about $30 to $40 billion per gigawatt. Compared to this figure, when you consider deploying AI 200 or AI 250 chips in inference scenarios, what is your expected cost or cost-effectiveness target? In other words, can you help us understand where Qualcomm's cost advantage lies in deployments of the same scale? Additionally, specifically regarding cooperation with Humain, what kind of revenue contribution would deploying 200 megawatts of computing power bring?

A: I will provide as much information as possible without revealing too many details that will be announced early next year. First, regarding revenue expectations, we originally expected significant revenue growth in the data center business to begin in FY2028. However, thanks to cooperation with Humain and our progress on AI accelerators, we now move this timeline forward by one year to FY2027, when data center business revenue will start to become significant.

Secondly, we are gaining widespread market attention. In the current context of data centers facing power consumption and computing density constraints, many companies needing large-scale AI inference computing power deployment are showing strong interest in our solutions. It is certain that if our solution were not competitive, there would not be so many in-depth discussions. But specific platform KPIs will be detailed when we update the roadmap early next year.

Q: The market still seems very concerned about the performance in the March quarter next year, mainly because of the change in your share with that major Android customer. Historically, your mobile business has typically seen a high single-digit (e.g., 7-9%) quarter-over-quarter decline from the December quarter to the March quarter. Considering the reduced share, does this historical quarter-over-quarter decline trend still apply, or should we expect a different decline?

A: We are not providing specific guidance beyond the first quarter at this time. But as you have seen, the strong business momentum we demonstrated at the end of FY2025 has already been reflected in our just-released results and guidance for the December quarter, and this momentum is expected to continue throughout the fiscal year. The only additional reminder is that we expect to complete the acquisition of Alphawave in Q1 2026. Other than that, as you mentioned, our business momentum remains strong.

Q: You mentioned that the performance in the September quarter exceeded expectations mainly driven by high-end Android business, but it seems more like it came from your largest customer (Samsung). You previously hinted that due to reduced share, revenue from that customer would decrease by about $500 million, but the financial report shows it was far less, with only a slight year-over-year decline. Can you explain this discrepancy? Also, as part of this question, can you reveal the baseline assumption for that customer's business volume in the December quarter guidance?

A: Our previous expectation was that in the newly released phone, we would occupy three out of four models, and that was indeed the case. The final actual share, of course, depends on market sales.

Specifically, for the September quarter, the performance guidance we provided already considered demand from that customer (Samsung). Therefore, the quarter's performance exceeding expectations was not driven by Apple but by other Android customers, particularly high-end models using our new Snapdragon chips.

Looking ahead, for the December quarter, we expect QCT's mobile business revenue to achieve approximately 11%-13% (low teens) quarter-over-quarter growth. This growth is also mainly driven by the Android business. Although there is some contribution from the Apple business, the core driver of quarter-over-quarter growth is indeed the shipment of high-end Android models.

Q: Is there any new progress in the patent licensing negotiations with Huawei? It seems like these negotiations have been dragging on for a while. Can you talk about the current situation?

A: We currently have no new progress to announce. Discussions between the parties are ongoing, but beyond that, there is no more substantive information to share.

Q: QCT revenue excluding Apple business grew 18% year-over-year. Even if I exclude automotive and IoT businesses, it's clear that the Android smartphone business achieved very strong double-digit year-over-year growth. Considering that Android smartphone shipments themselves did not grow that much, can it be assumed that this revenue growth is almost entirely driven by increased per-unit value? Looking ahead, should we continue to use this content-driven growth rate as the correct reference standard for evaluating your business?

A: There are two main drivers behind this growth. First, is the shift in product mix towards high-end. This is a trend we have observed continuously over the past few years, and it is not limited to developed markets but also applies to emerging markets. The grade of devices consumers are purchasing is continuously improving, which directly benefits our revenue. Second, is the growth in per-unit value (content) within the high-end tier. As we launch increasingly powerful chips, phone manufacturers can deliver more powerful phones, allowing us to continuously increase the value we derive from each high-end device.

Q: You mentioned the strong performance of the Snapdragon Android business in the September and December quarters, is this strength mainly coming from the Chinese market? Is this simply due to the timing of new product launches, or is there a situation of customers pulling in orders ahead of time? For this strong momentum, should we consider any potential risks or special factors?

A: No, there is no situation of pulling in orders ahead of time. What we observe is that almost all of our major Chinese customers have released new models, and the initial market response to these devices has been very positive.

Additionally, later this quarter and early next year, we will also see many global customers releasing new devices one after another. So, the strong momentum you see is simply reflecting the normal procurement pattern after new product launches and the enthusiastic initial market response to these new products.

Q: According to the information in the press release, your product architecture—such as using DDR memory and PCI Express interfaces—seems different from the solutions adopted by other market participants. How should we interpret this? Is this just Qualcomm's 'first step' into the market, with more iterative products to follow? Or does this represent a completely different philosophy in your market approach—focusing more on energy efficiency as you mentioned? In summary, is this a differentiated approach that is completely different from the current market mainstream?

A: Yes. Our starting point for thinking about this issue is 'what should the future AI architecture look like'. This way of thinking applies not only to data centers but also to the edge computing field where we have long been involved. When we focus on building dedicated inference clusters, our goal is very clear: to achieve the highest computing density with the lowest cost and power consumption, thereby efficiently generating tokens. Under this goal, we believe there is a better architecture that can surpass the traditional GPU plus HBM memory combination. This is the direction we are striving to develop. We must successfully execute this strategy, and this is also the current core focus of the company.

Q: To what extent is the growth you see in the mobile business driven by the increase in the average selling price of Snapdragon chips themselves? Clearly, as you adopt more advanced processes, wafer costs are also rising. Can you talk about how much the increase in chip ASPs is impacting your current and future mobile business growth? Additionally, how is the entire mobile industry digesting and absorbing this ASP increase?

A: We have observed a long-standing trend, a question we discuss almost every year. There is always very strong demand in the market for more powerful, higher processing capability flagship chips. The driving force behind this comes from two aspects: one is the fierce competition among phone manufacturers, and the other is consumers' desire to achieve more functions on their phones. We have a clear plan for our future generations of chips and have entered into in-depth discussions with customers, so we are very confident that this trend of continuous growth in per-unit value will continue in the coming years.

Additionally, it is important to remember the second important factor I emphasized earlier: the devices consumers are purchasing are significantly shifting towards higher-end models. This does not refer to value growth within the flagship tier but rather that more and more consumers are choosing to purchase higher-grade phones. This is also a long-term trend we have observed for many years and expect to continue.

Q: This quarter's mobile business grew by 14%, and according to your guidance for the next quarter, QCT's growth expectation seems to be 600 basis points higher than the market. Can you specifically analyze the components of this 'outperforming the market' for the next quarter? Can you talk about the expected performance of the mobile, IoT, and automotive business segments? Compared to the initial expectations of the last quarter, which parts do you think will perform better? Please introduce the growth drivers of each QCT business segment for the next quarter.

A: Automotive Business: We set a record of approximately $1.1 billion in revenue in the September quarter. For the next quarter, we expect to be flat or slightly up. As more new cars equipped with our technology hit the market, we are in a very favorable position and will continue to grow throughout the fiscal year.

IoT Business: The situation is similar. The performance in the September quarter has significantly exceeded our previous guidance, and we expect IoT business revenue to continue to grow throughout the rest of the fiscal year starting from the first quarter.

Mobile Business: The growth expectation you see in the December quarter is mainly due to the successful launch of our next-generation flagship chip. All major phone manufacturers (OEMs) have launched devices equipped with this chip and have received strong consumer market responses, which is already reflected in our financial forecasts. As I mentioned earlier, we expect QCT's mobile business revenue to achieve 'low double-digit' quarter-over-quarter growth.

Q: Historically, when your new products are released in the Chinese market and coincide with the New Year and Chinese New Year consumption seasons, does this usually mean that the company's first fiscal quarter (i.e., October to December) is typically the strongest quarter of the year? From a seasonal perspective, what trends usually appear in the following quarters?

A: We expect the company's first and second fiscal quarters to be the stronger quarters of the year. And typically, the third fiscal quarter, which includes June, will be a relatively low point. Therefore, in terms of mobile business, its seasonal trend should remain consistent with the patterns you have seen in the past.

Q: QCT's revenue grew 5% year-over-year this quarter, but the profit margin fell by more than 100 basis points. I want to understand the reason behind this decline: is it mainly due to changes in the product mix, or is it because of rising manufacturing costs? Or is this simply the result of increased R&D investment to achieve future revenue growth?

A: When you examine the year-over-year trend in profit margins, you should recognize that we are making focused investments in the data center field. Over the past few years, we have been committed to shifting operating expenses from mature businesses to high-growth areas. And now, the data center business is an additional investment focus in our overall investment blueprint, which has impacted the current profit margin performance.

Q: Further focusing on your non-Android mobile business. Do you have any new guidance or information you can share on how we should model this business's performance in the 2026 calendar year?

A: Our view on the share we hold in Apple's business has not changed and remains completely consistent with what we have said in the past.

Q: I remember the XR business was set at $2 billion, the smallest among the opportunities listed at the time. If you plan to hold a dedicated event for the data center business and provide updates, does this mean that the potential scale of the data center business will be significantly larger than what was presented at the last Analyst Day? Can we expect it to become another multi-billion-dollar major opportunity? Can you clarify this for us?

A: We see the market, especially the AI smart glasses market, taking off very quickly. Therefore, we do feel that the current development has significantly outpaced the guidance previously provided, and we see tremendous upside potential.

More broadly, if personal AI is viewed as a broader opportunity—whether realized through glasses, watches, or ear-worn devices, etc.—this could evolve into a very large market. If the market develops as we expect, it will create enormous commercial upside.

It can be confirmed that the potential scale of the data center business will be higher than that number. We believe that if we succeed in this field, it is expected to bring us a multi-billion-dollar new revenue opportunity in the coming years. This is our current view on this matter.

<End Here>

Risk Disclosure and Statement of this Article:Dolphin Research Disclaimer and General Disclosure