TCOM 4Q25 First Take: Results were solid, with both strengths and weaknesses. The highlight is revenue growth beating prior guidance across the board, with a clear acceleration.

A minor weakness is expenses ramped meaningfully, especially marketing, pushing GAAP OP below expectations. Given limited disclosure in the release and the market's focus on recent regulatory issues and potential impact, please refer to the upcoming Trans for more detail.

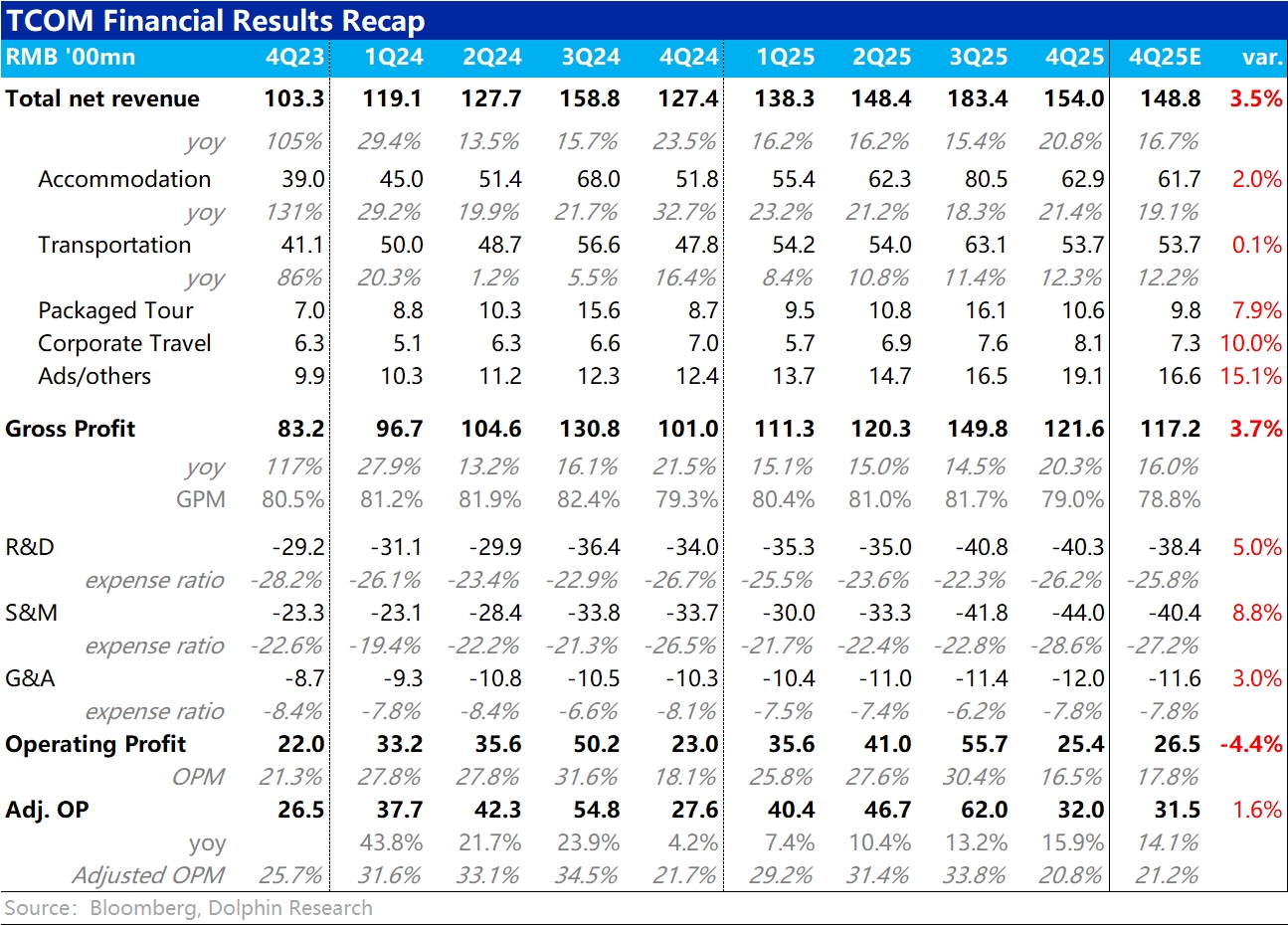

Quarter details: Key points below.

1) Total revenue rose nearly 21% YoY, a clear step-up from 15% last quarter and well ahead of guidance and Street. By biz. line, growth picked up across segments. Outperformance came mainly from package tours and Ads & Other, two smaller lines that surprised on the upside.

2) Alongside strong topline, total opex growth accelerated to 23% YoY despite a tough base, outpacing revenue. The main driver was marketing spend, up 30%+.With JD and Fliggy stepping up, while unlikely to dent TCOM's share, they likely raised traffic acquisition pressure, resulting in GAAP OP coming in ~4% below expectations. More detail will be in the upcoming Trans.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.