XPeng 4Q25 First Take: Overall, headline results looked strong, with revenue, GPM and profit beating expectations. Net profit turned positive for the first time since listing, in line with prior guidance.

Peel back the sheen, though, and underlying performance in the core auto biz and the forward guide point to mounting pressure. The outlook reads cautious.

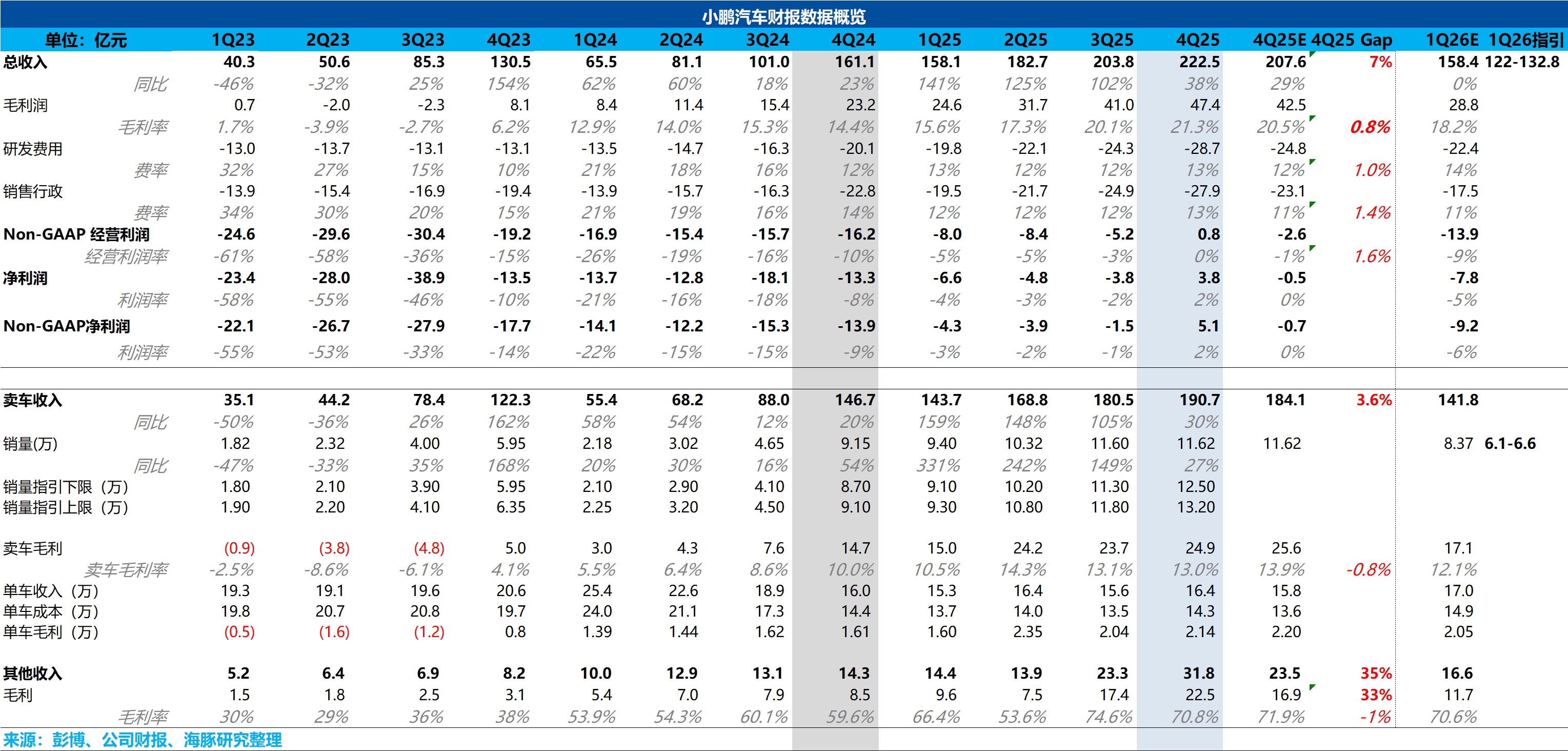

① High-margin services and Gov. subsidies flattered core auto weakness; revenue beat was driven by 'VW collaboration' and carbon-credit income boosting services/other: Total revenue reached RMB 22.3bn (vs. RMB 20.8bn est.).

Auto sales revenue was RMB 19.1bn (+30% YoY, vs. RMB 18.4bn est.), helped by mix upgrade from higher X9 contribution lifting ASP, and a rising share of higher-ASP export models. The largest upside came from 'services and other' revenue.

It jumped QoQ by RMB 0.85bn to RMB 3.2bn (well above the RMB 2.35bn est.). We estimate this reflects milestone recognition from the E/E architecture R&D services with Volkswagen, plus carbon-credit gains tied to export growth.

② Core auto gross margin missed: Total GPM was 21.3% in Q4 (+120bps QoQ, vs. 20.5% est.), lifted mainly by high-margin tech services. By contrast, the core auto sales GPM was just 13%, roughly flat QoQ and below the 13.9% consensus.

Despite a higher mix of the margin-richer X9, auto GPM failed to meet expectations. Rising per-unit manufacturing costs — early supply-chain/capacity ramp costs and higher battery costs — likely offset mix benefits.

③ Positive net profit lacks quality; core operations still bleeding: While net profit turned positive, it relied heavily on RMB 0.84bn of 'other gains' (mainly one-off Gov. subsidies). Ex these non-recurring items, XPeng would still have posted a net loss in Q4.

On a more telling basis of core operating profit (GP minus core Opex), Q4 was RMB -0.93bn, worse than Q3's RMB -0.82bn. Despite higher GP QoQ, a sharp QoQ increase in S&M, G&A and R&D (the three Opex lines) capped profit release.

Most importantly, the 1Q26 guidance. It is the key focus.

④ Guidance under the 'one model, two powertrains' launch cycle fell short: It disappointed vs. expectations.

Versus Q4's mixed print, the 1Q guide is notably weak. The tone is soft.

Delivery guide is weak, failing to show a new-model surge: 1Q deliveries are guided to 61k–66k, well below the 84k the market expected. With Jan (~20k) and Feb (~15k) known, the implied Mar run-rate is only 26k–31k.

Given dense 1Q launches of G6/P7+/G7/X9 range-extended 'super' trims plus annual refreshes for BEVs (the full rollout of the 'one model, two powertrains' strategy), this pace suggests the new-model effect is underwhelming vs. expectations.

Revenue guide implies ASP pressure; price war bites. 1Q revenue is guided to RMB 12.2bn–13.28bn. Ex services/other, the implied ASP is roughly RMB 155k–165k per vehicle, with the top end only flat vs. Q4 and below the RMB 170k the market expected.

Even with a further mix lift from the high-end X9, overall ASP still falls short, likely due to heavier promotions and discounting. $XPeng(XPEV.US) $XPENG-W(09868.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.