XPEV: All Hype, No Profits — Still the 'Tesla of the East'?---

$XPeng(XPEV.US) released Q4 2025 results after HK close and before US market open on Mar 20, 2026 (Beijing time). Headline numbers looked solid, but guidance for the core auto biz signaled pressure. Details below:

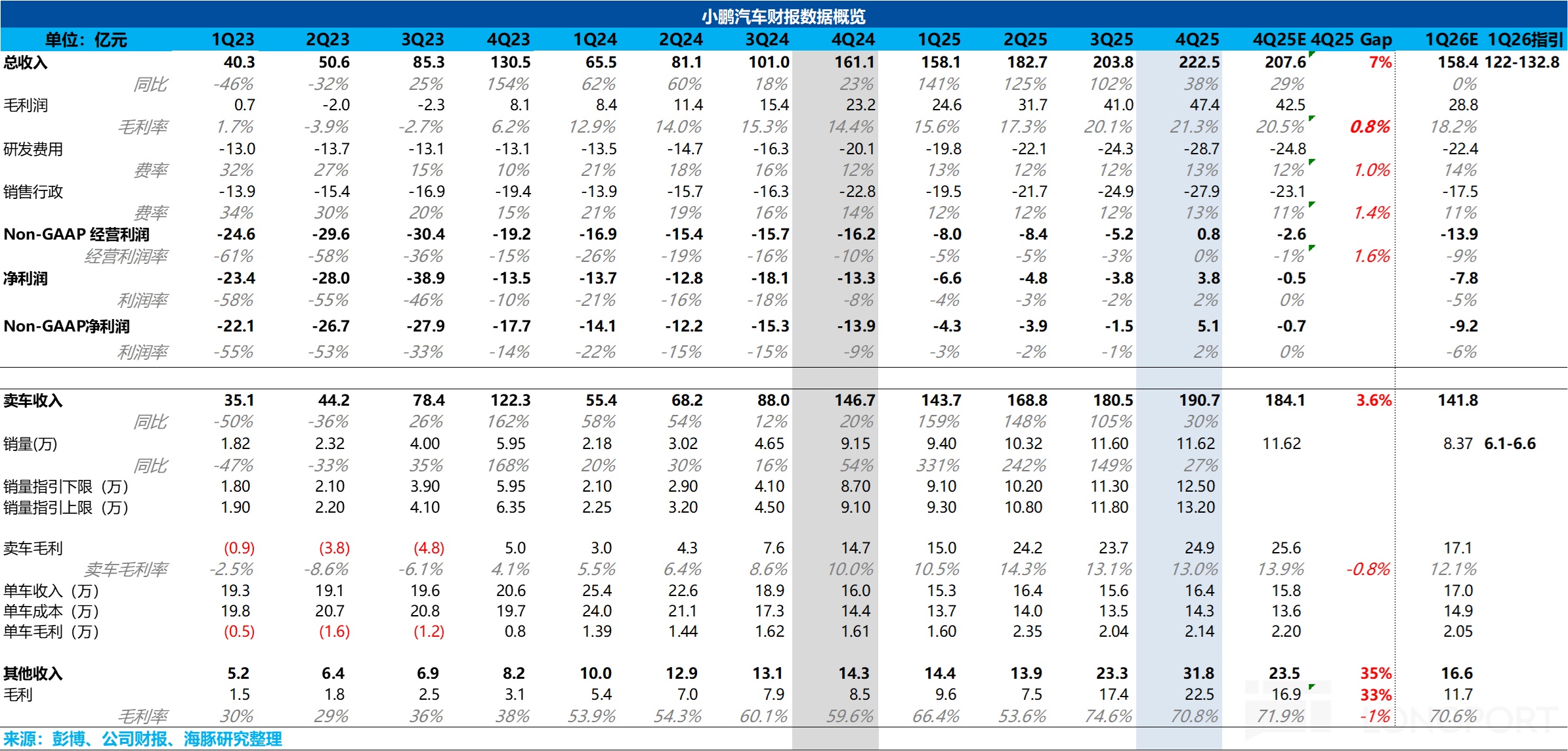

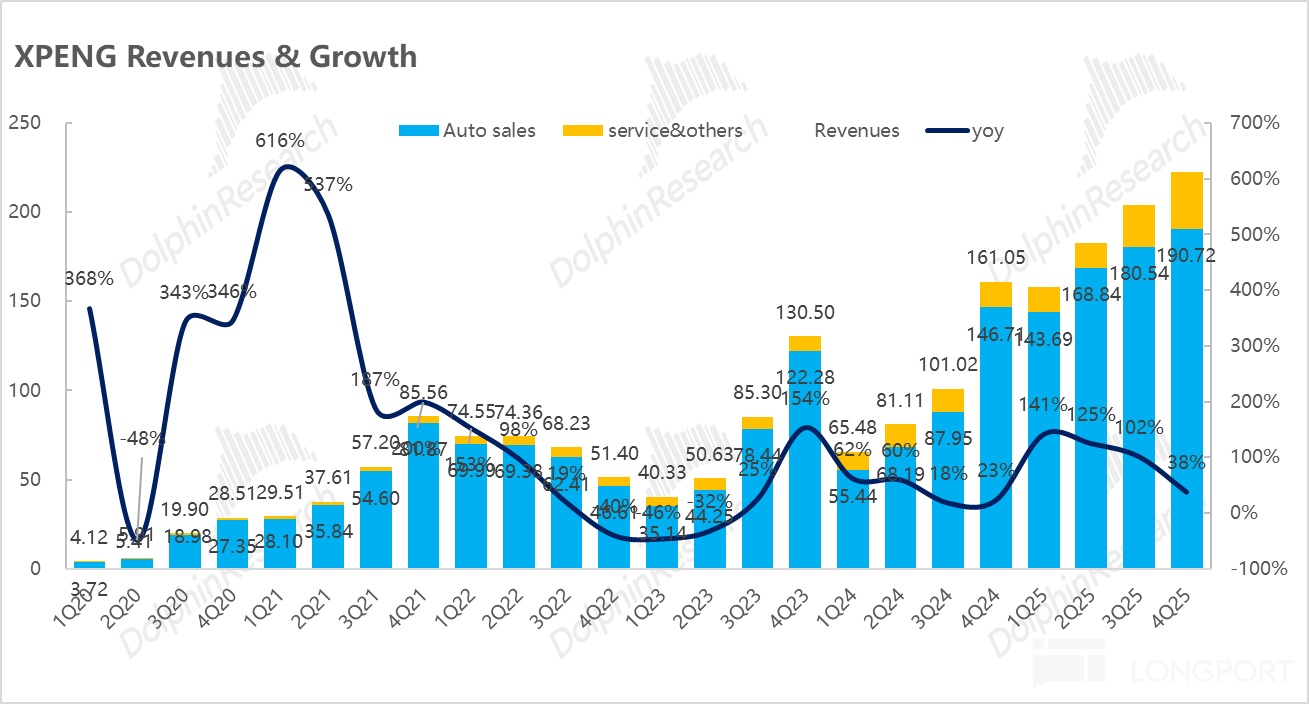

1) Revenue beat driven by services & other: Total revenue came in at RMB 22.3bn (+38% YoY), above the street at RMB 20.8bn. The upside vs. consensus was material.

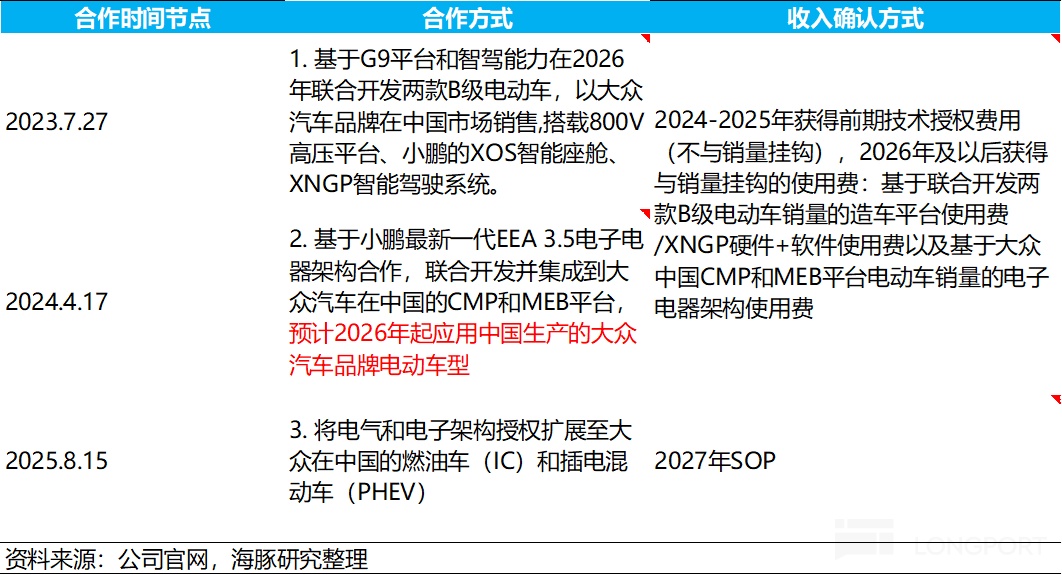

The biggest delta was 'services and other revenue', which surged QoQ by RMB 850mn to RMB 3.2bn, well ahead of the RMB 2.35bn consensus. This mainly reflected milestone-based E/E architecture R&D revenue recognized from the Volkswagen collaboration and extra carbon-credit income as exports scaled.

2) Auto revenue up QoQ on mix: Auto sales were RMB 19.1bn (+30% YoY), topping the RMB 18.4bn consensus. This was driven by a higher mix of the higher-ticket X9 and the contribution from higher-ASP export markets.

3) But unit economics did not improve at the GP level: Vehicle GPM was 13%, flat QoQ and below the 13.9% street estimate. Despite the richer mix, higher unit costs (likely from lack of scale plus supply-chain and ramp costs) offset the mix benefit.

4) Overall GPM beat was highly mix-dependent on high-margin 'services & other': Consolidated GPM reached 21.3% vs. 20.5% expected, helped by the naturally higher margins of tech licensing and carbon credits. 'Other & services' posted a 70.8% GPM and contributed RMB 2.25bn of GP, meaning just 14% of revenue delivered nearly half of total GP, far above the RMB 1.7bn market expectation.

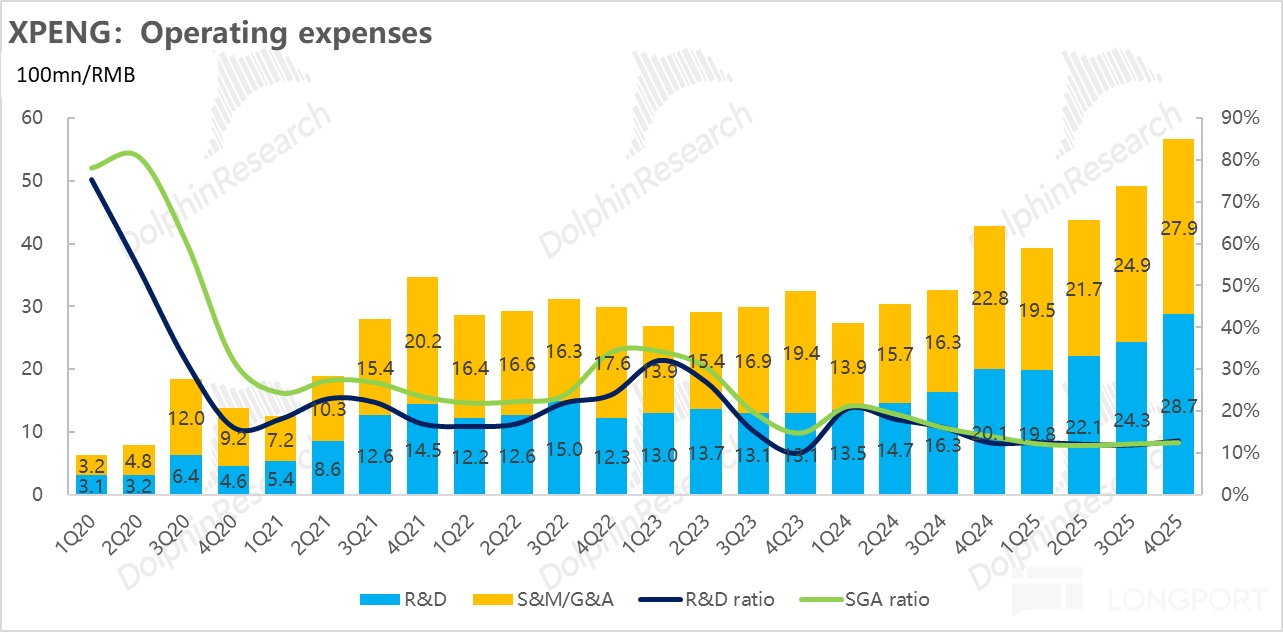

5) Opex jumped QoQ to fund the 'dual-powertrain per model' strategy and AI: XPeng front-loaded spend for a 2026 product super-cycle and AI, pushing both R&D and S&M well above expectations. This was deliberate investment.

R&D reached RMB 2.87bn, far above the RMB 2.48bn street, driven by a dense new product cycle, autonomous driving, and humanoid robotics. Sales expenses were also RMB 2.79bn vs. RMB 2.3bn expected, reflecting front-loaded marketing and channel build-out for the 'one model, BEV + super range-extender' strategy.

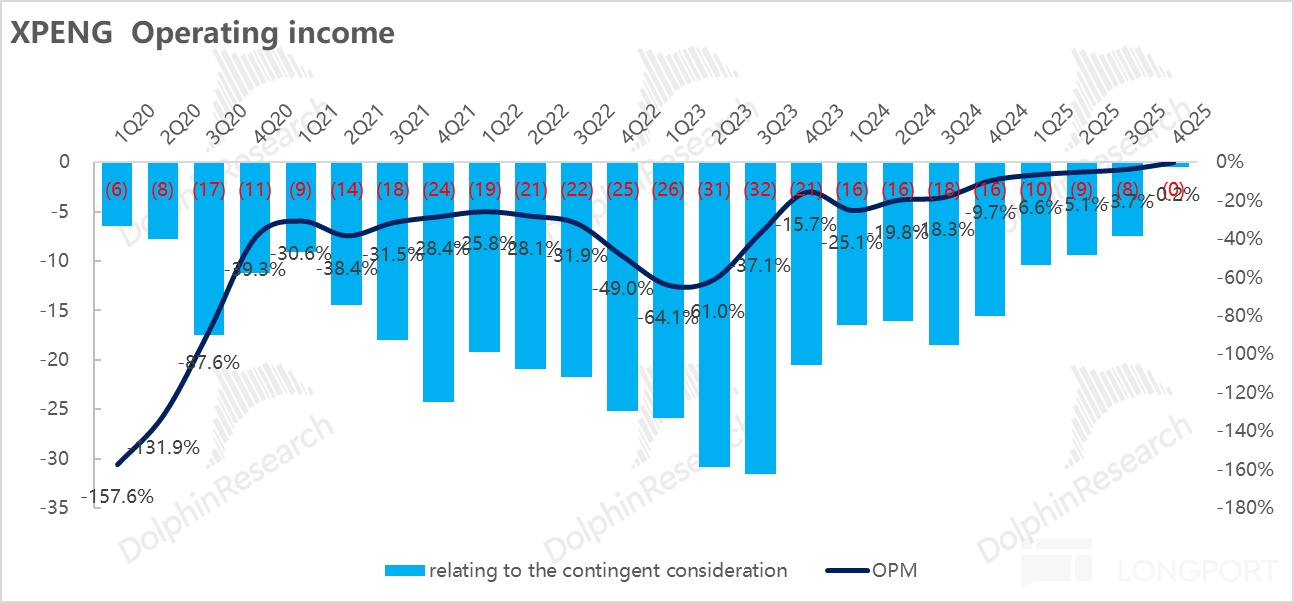

6) Positive net profit lacks quality as core ops still bleed: Net profit was RMB 380mn, the first positive quarter since listing. But it relied heavily on RMB 840mn of one-off 'other income' (mainly subsidies), and profit would still be negative excluding these.

Core operating profit (GP minus core Opex), a better gauge of self-funding ability, was -RMB 920mn in Q4 vs. -RMB 820mn in Q3, widening by ~RMB 100mn QoQ. Rising GP was more than absorbed by sharply higher R&D and S&M, implying the core biz remains in the red.

Dolphin Research view:

On the surface, Q4 was strong: revenue, GPM and net profit all beat, and net income turned positive for the first time. Optics were good.

Strip that back, however, and high-margin tech services and sizable subsidies inflated reported profitability, while core auto saw 'more revenue, no more profit' in Q4. What the market cares more about is XPeng’s soft 2026 guidance and whether there is a credible path to break out.

① On the critical Q1 2026 guide:

Under the 'one model, dual powertrains' cycle, guidance fell short, pointing to heavy sell-through pressure: The tone was cautious. Sell-through remains the key swing factor.

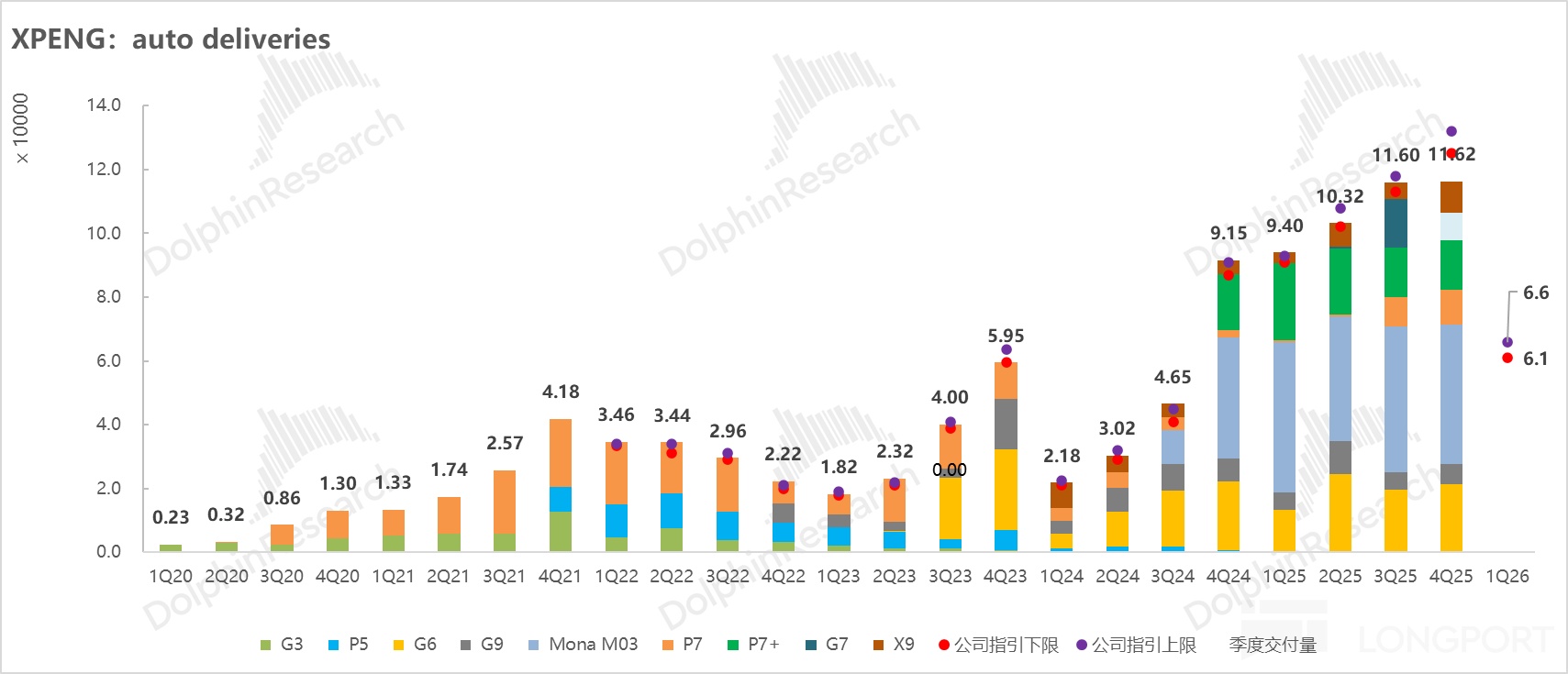

a. Volume guide is weak, failing to show a new-model pop: Q1 deliveries guided to 61k–66k units (-30% to -35% YoY), well below the street at 84k. Based on known Jan (~20k) and Feb (~15k) prints, the implied Mar run-rate is 26k–31k, a recovery but not strong enough.

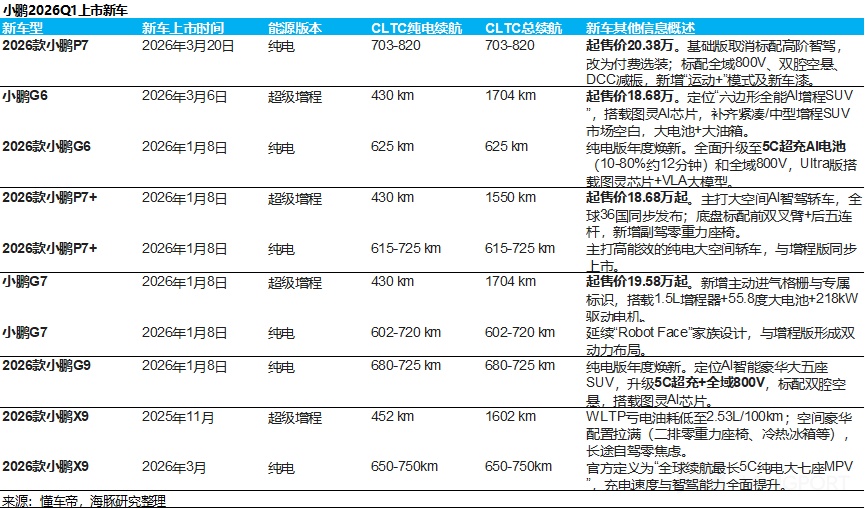

Despite seasonal softness and the drag from purchase tax step-down, XPeng launched the BEV + super range-extender lineup across G7/P7+/G6/G9. With aggressive 'range-extender at BEV price' and 'spec bump at same price' positioning, these long-range variants (430km BEV range/1,550km+ combined) started deliveries in late Jan but did not trigger the expected demand spike, raising questions around cycle elasticity.

b. Revenue guide implies lower ASP; vehicle GPM likely stays under pressure:

Q1 revenue is guided to RMB 12.2bn–13.28bn. Excluding services/other, the implied ASP is ~RMB 155k–165k, with the high end only flat QoQ and below the ~RMB 170k street.

Even as the X9 mix is expected to rise, ASP still lags. This likely reflects heavier promotions and price cuts, making the sell-through pressure visible.

With ASP pressured by discounts, Q1 vehicle GPM also faces two cost headwinds:

1) Scale deleverage: sharply lower deliveries QoQ lift per-unit D&A and fixed costs. 2) Upstream inflation: battery, memory chips and aluminum prices have been rising.

② For full-year 2026:

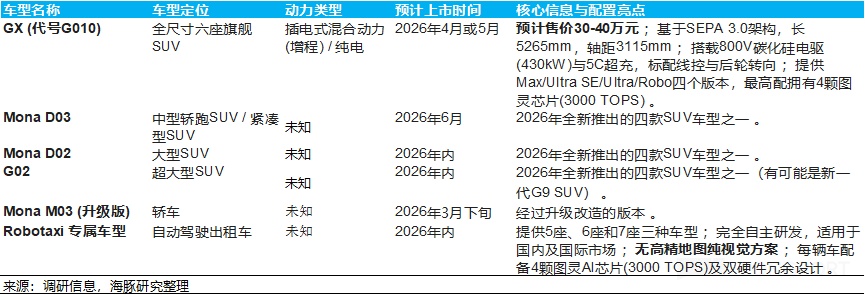

Despite a soft Q1 start and no formal FY26 delivery target yet (watch the call), the market still models 520k deliveries (+21% YoY). Growth is expected from the super range-extender lineup and four new SUVs planned for 2026 (including Mona D02, Mona D03, GX and G02/G01).

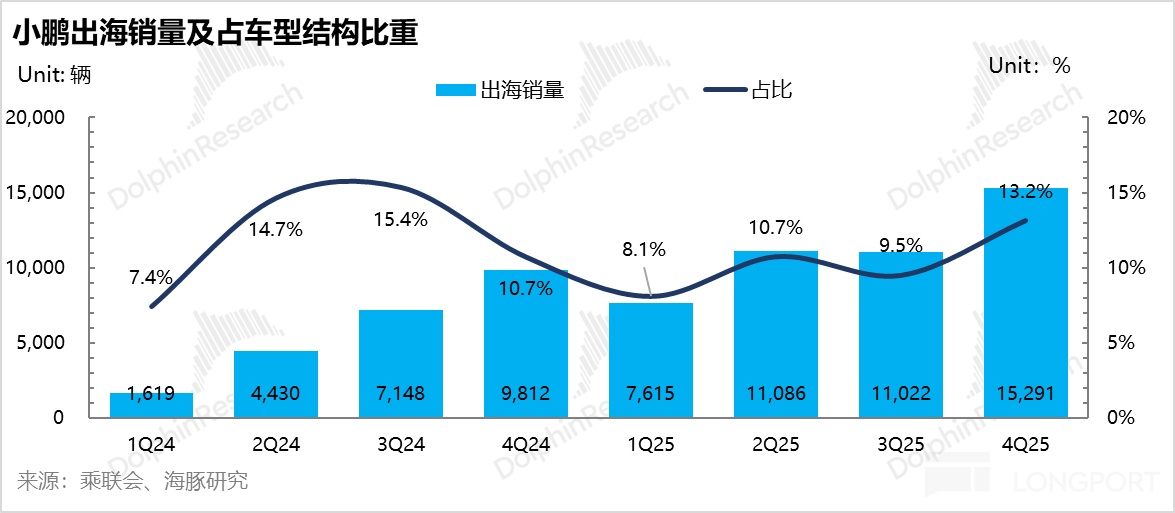

Exports as the core growth engine: Management previously planned to double overseas sales to 90k units in 2026 (45,006 units in 2025). XPeng will focus on Israel, Germany, Norway, Thailand and France, with at least four of six global core models launching, and expand its network to 680 stores across 60+ countries/regions.

The longer-term target is >1mn overseas units by 2030, contributing >70% of total profit. With 7k exports in Jan–Feb (annualized ~42k), this aggressive target still needs to be proven.

Domestic base supported by a 'major new-model cycle':

If the 90k export target is met, the 520k total implies 430k domestic units (+12% YoY). Given two Mona platform volume SUVs launching in Q2 and 2H, hitting this looks plausible.

On AI: XPeng is accelerating from R&D to commercialization:

a. Autonomy stack upgrade: On hardware, the self-developed 'Turing' chip with 750 TOPS per die is now in mass production on new models. On software, XPeng launched its second-gen vision-language-action model 'VLA 2.0' in Mar 2026, using a 'vision + language to action' architecture to map vision directly to control and reduce latency.

To speed convergence, XPeng formed a 'General Intelligence Center', integrating ADAS and smart-cabin teams under one AI base model. This aims to unify stack development.

b. Robotaxi ramp: XPeng plans three Robotaxi-focused models (5/6/7-seat) in 2026. They operate without HD maps, rely on vision, use four Turing chips (3,000 TOPS) and dual hardware redundancy, with pilots in 2026 and SDK licensing to third parties.

c. Humanoid robot push: The next-gen 'Iron' humanoid uses solid-state batteries and three Turing chips (2,250 TOPS), integrating VLT, VLA and VLM. Mass production is targeted by end-2026, with initial use cases in guiding and shopping assistance.

Valuation: XPeng trades around 1.3x FY26E P/S. Given softer guidance, the market may reassess the 'dual powertrains per model' cycle; without a constructive 2026 delivery guide, the stock may face further near-term downside.

Longer term, XPeng’s AI execution is among the leaders, and four new SUVs in 2026 (notably Mona volume models) provide optionality. It remains a potential breakout name.

On Dolphin’s conservative case of 500k 2026 deliveries (+16% YoY) and ~RMB 92bn revenue, we assign 1.0–1.2x P/S, implying RMB 92bn–110bn mkt cap as an attractive entry to capture 'auto + AI' value, with a better margin of safety. This largely prices only the core auto biz, excluding AI options from Robotaxi and robots.

Full analysis follows:

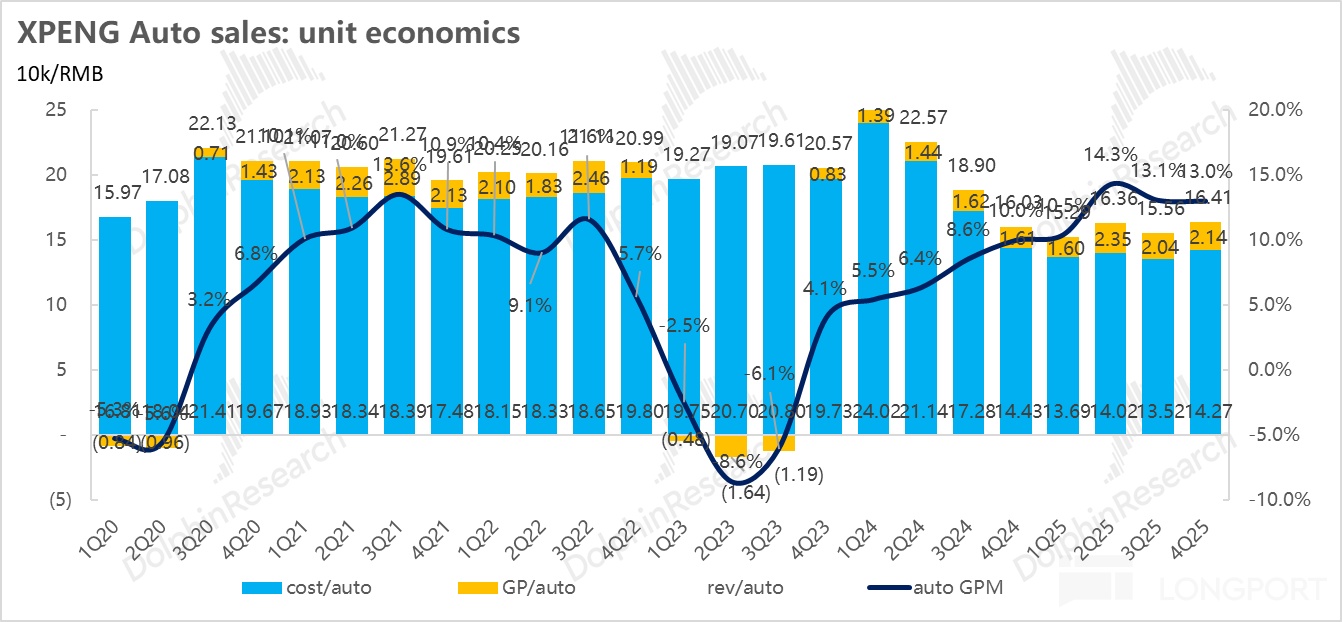

I. Vehicle GPM missed expectations

With Q4 deliveries already disclosed, investors focused on auto revenue and margins. The watchpoint was the vehicle GPM trajectory.

Deliveries were roughly flat QoQ, and the market expected vehicle GPM to tick up from 13.1% in Q3 to 13.9% on better mix. Instead, Q4 vehicle GPM printed 13%, essentially flat QoQ and below consensus.

While mix uplift supported ASP, unit costs rose sharply in tandem, fully offsetting mix benefits. This explains the GPM miss.

By unit economics:

a) ASP: higher-priced models and exports drove an ASP beat

Q4 ASP reached ~RMB 164k, up ~RMB 8k from ~RMB 156k in Q3, above both the ~RMB 158k street and the prior implied guide of ~RMB 155k. Two drivers stood out:

① Higher X9 mix: The flagship X9’s share rose 4ppt QoQ to 9%, while the lower-price MONA M03 fell 2ppt QoQ to 38%. Domestic mix shifted toward higher price bands.

② Exports with higher margins kept scaling: Export volume reached 15.3k units, taking mix up 3.7ppt QoQ to 13.2%. Given higher overseas pricing, this lifted overall ASP.

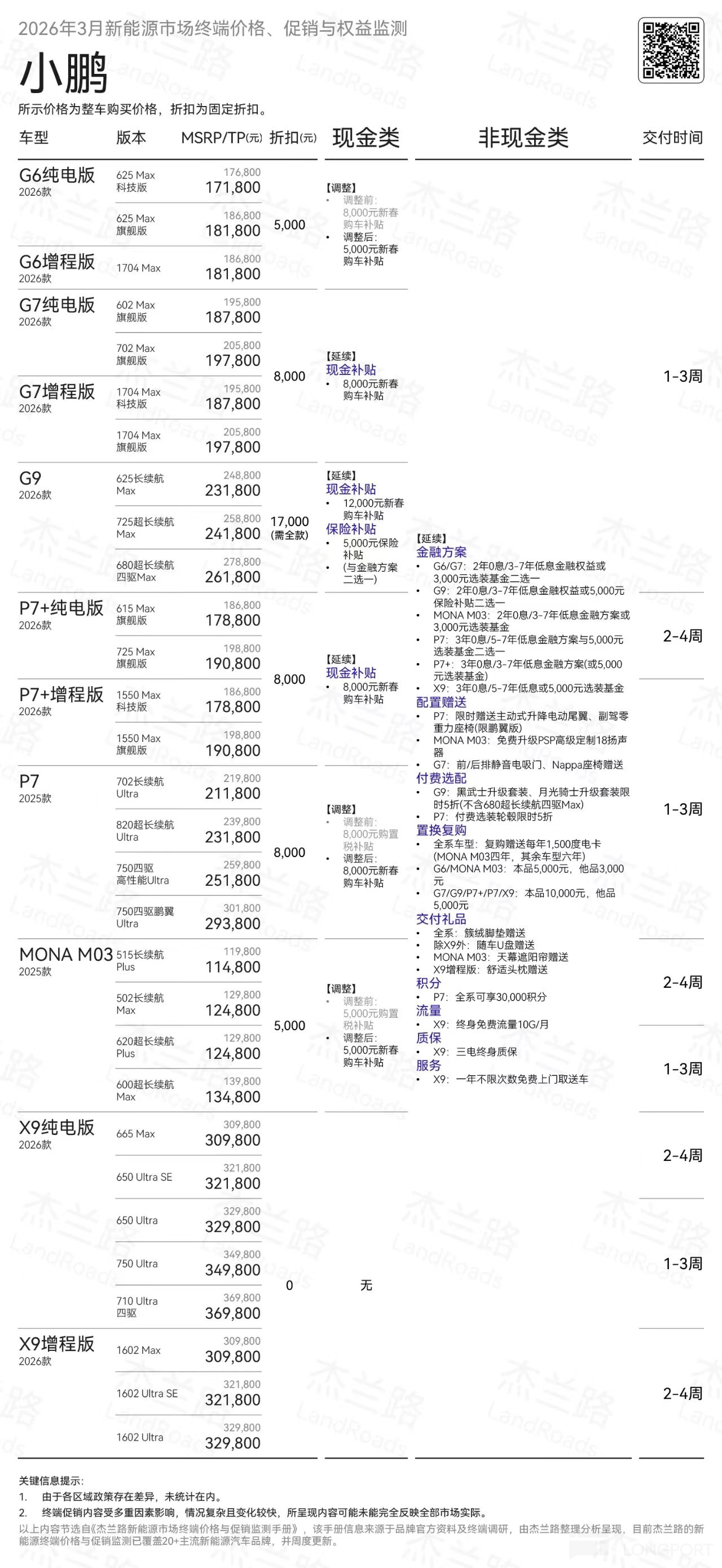

③ Discounting was contained:

In Q4, XPeng offered cash discounts of RMB 5k/5k/15k for G6/G9/X9 BEV, and maintained 3-year 0%/5-year low-rate plans for some models. Overall discount intensity was manageable, limiting ASP drag.

b) Unit cost: lack of scale drove a sharp cost increase and weighed on GPM

Unit cost rose to ~RMB 143k from ~RMB 136k in Q3, up ~RMB 7k QoQ. This was the primary headwind on margins, driven by:

① Intrinsically higher costs on premium models: A bigger X9 mix raises the BOM given its large MPV form factor. Higher materials are inherent.

② Scale benefits stalled: Q4 deliveries were only ~116k units, flat QoQ and below the 125k–132k guide. Stagnant volume limited fixed-cost absorption for plant D&A and overheads.

The shortfall reflected state/local subsidy step-downs around late Q4 2025, which pulled forward price-sensitive demand into Q3, hurting volume models like MONA M03. Meanwhile, G7 and the new P7 averaged only ~2k units/month in Nov–Dec, failing to fill the gap.

③ Early ramp and supply-chain volatility: Initial ramp costs for new models (especially first-time super range-extender variants) and short-term battery component cost swings also pushed unit manufacturing costs higher. This compounded the pressure.

c) Unit GP: 'more revenue, no more profit' left GPM flat

Unit GP was ~RMB 21k, up only ~RMB 1k QoQ and below the ~RMB 22k street. As a result, vehicle GPM was 13%, flat QoQ and below the 13.9% consensus.

II. Guidance under the 'dual powertrains per model' cycle fell short

Versus a mixed Q4, Q1 guidance skewed weak. This underscores demand risk.

a) Volume guide is soft, with no visible new-model spike:

Q1 deliveries of 61k–66k imply -30% to -35% YoY, far below the 84k street. With Jan at ~20k and Feb at ~15k, implied Mar is 26k–31k, showing a rebound from Feb but modest.

Q1 is seasonally weak and the purchase-tax step-down adds pressure, yet XPeng deployed G7/P7+/G6/G9 across BEV and super range-extender. Each range-extender uses a 1.5T generator with CLTC BEV range of 430km and combined range of 1,550–1,704km.

Even with 'range-extender at BEV price' and 'spec bump at same price', and deliveries from late Jan, the expected demand pop did not materialize. This raises doubts about the current cycle’s firepower.

b) Revenue guide implies ASP pressure; sell-through remains tough

Total Q1 revenue is guided to RMB 12.2bn–13.28bn. Ex-services, implied ASP is ~RMB 155k–165k, with the top end only flat QoQ and well below the ~RMB 170k street.

Even with higher X9 mix, ASP fails to break higher, likely due to heavier terminal promotions and price cuts. Sell-through pressure is evident:

① Cash cuts: RMB 5k on MONA M03 and G6; RMB 8k on P7+, old P7 and new G7; and up to RMB 17k on the premium BEV SUV G9. ② Extended financing: the 7-year low-rate program across the lineup lowers the purchase hurdle.

With ASP under pressure, costs are rising, so Q1 vehicle GPM likely faces heavy headwinds:

① Scale deleverage: lower QoQ volume drives per-unit fixed-cost inflation. ② Upstream inflation in batteries, memory, aluminum and other inputs continues.

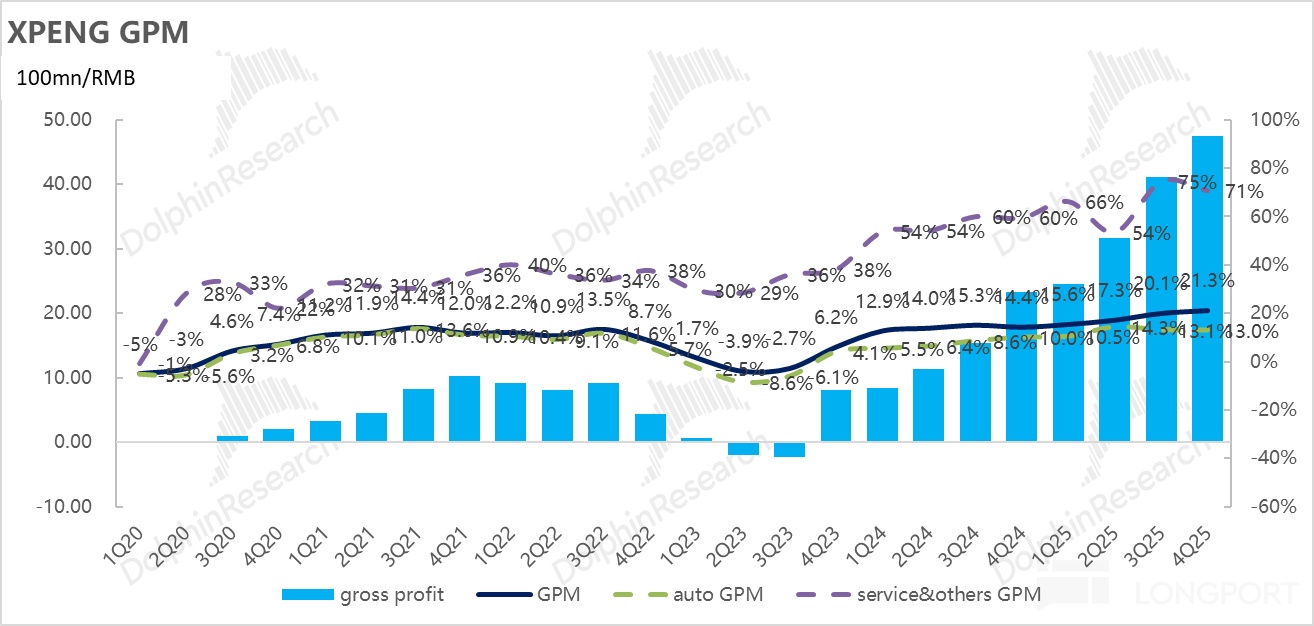

III. Overall GPM beat: Volkswagen tech licensing and carbon credits polished reported profits

Q4 revenue was RMB 22.3bn (vs. RMB 20.8bn est.), and overall GPM was 21.3% (vs. 20.5% est.). But the beat was not from core autos.

① Revenue beat leaned on services & other:

Core autos: revenue up, but GPM did not follow

Auto revenue at RMB 19.1bn (+30% YoY) benefited from higher X9 mix and exports, but high unit costs erased mix gains, leaving vehicle GPM at 13%, below expectations. This muted core profitability.

Services & other: revenue spike from tech licensing and carbon credits

'Services & other' jumped QoQ by RMB 850mn to RMB 3.2bn, far ahead of the RMB 2.35bn street. Key drivers were VW E/E architecture milestones and higher export-linked carbon-credit revenue.

② GP mix masked core profitability

With the structurally high margins in licensing and carbon credits, 'services & other' posted a 70.8% GPM (down ~4ppt QoQ on mix but still very high), contributing RMB 2.25bn GP vs. ~RMB 1.7bn expected. At just 14% of revenue, it delivered nearly half of total GP, lifting consolidated GPM to 21.3%.

IV. Opex surged to build the 'dual powertrains' and AI stack, weighing on core earnings

XPeng treats 'intelligence' as its moat, requiring sustained heavy spend in AD and new platforms. That framework shaped Q4 results.

Front-loaded investment for the 2026 product year drove R&D and S&M above expectations, becoming the main drag on core OP. The step-up was intentional.

1) R&D: RMB 2.87bn, well above expectations, doubling down on new models and physical AI

R&D spend of RMB 2.87bn exceeded the RMB 2.48bn street and rose RMB 450mn QoQ from RMB 2.43bn. Key uses included:

① Pre-investment for a dense new product cycle: In Q4 2025, XPeng advanced its 'one model, dual powertrains' pivot, launching the X9 super range-extender. It is preparing range-extender variants for all BEVs and four new SUVs for 2026, driving platform, powertrain integration and validation costs.

② Autonomy upgrades: The in-house 'Turing' chip (750 TOPS/die) entered mass production on G7 and the new P7 from Q3. Algorithmically, VLA 2.0 (vision-language-action) launched in Mar 2026 with an end-to-end 'vision-to-action' architecture to cut latency and unify deployment across autos, Robotaxi, robots and eVTOL.

To accelerate, XPeng created a 'General Intelligence Center' merging AD and smart-cabin teams to build a unified AI base model. This aims to improve reuse and speed.

③ Forward investment in humanoid robots: The next-gen 'Iron' humanoid uses all-solid-state batteries, three Turing chips (2,250 TOPS), and a multimodal VLT/VLA/VLM system. To hit commercialization in Apr 2026 (guiding/reception) and mass production by end-2026, training, hardware and scenario testing likely ramped QoQ.

2) S&M: RMB 2.79bn, stepping up for new-model scaling

S&M reached RMB 2.79bn vs. the RMB 2.3bn street and RMB 2.49bn in Q3. This mainly reflected front-loaded marketing and channel expansion:

① Higher marketing and commissions: Launch campaigns for X9 super range-extender lifted promo spend, and franchise commissions rose QoQ. Both added to the run-rate.

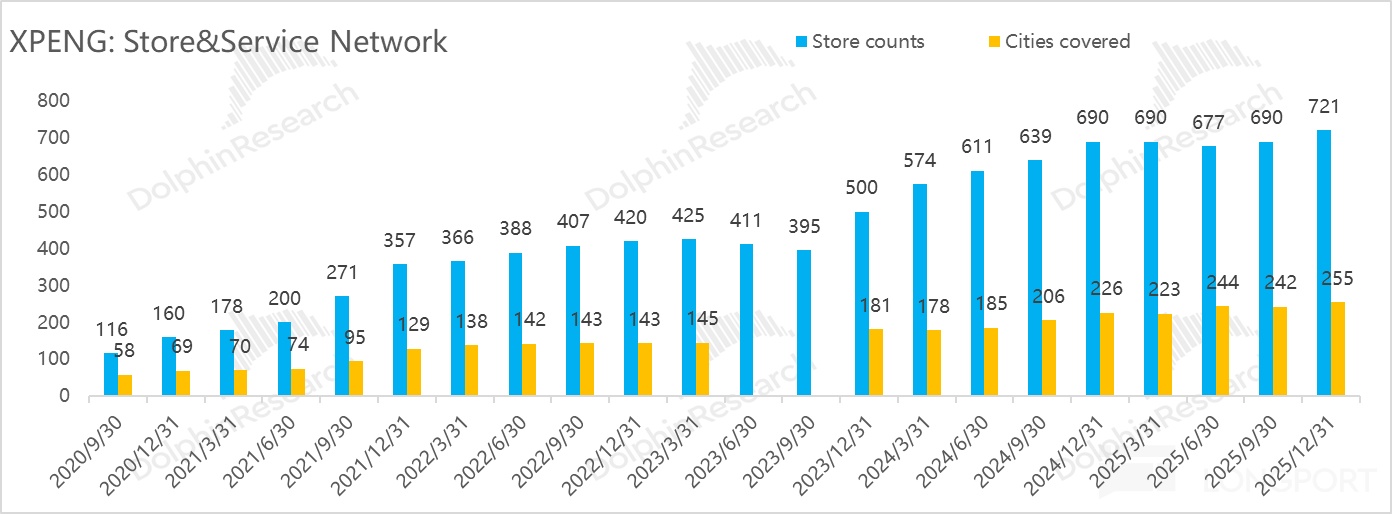

② Faster network build-out: To support the 2026 down-market push and four new SUVs, XPeng added 31 stores in Q4 (to 721) and entered 13 new cities (to 255). This raised rent and staffing costs sharply.

V. Net profit turned positive, but quality is low; core ops still loss-making

Q4 net profit of RMB 380mn is XPeng’s first positive quarter since listing, but it relied on RMB 840mn of 'other income' (mainly subsidies). Excluding these non-recurring items, XPeng would still be loss-making in Q4.

Core OP (GP minus core Opex) was -RMB 920mn vs. -RMB 820mn in Q3, widening by ~RMB 100mn. Despite higher GP, sharply higher S&M and R&D constrained profit release, leaving core ops in the red.

<End>

Past Dolphin Research deep-dives and updates on XPeng include:

Earnings season

Aug 19, 2025 review 'XPeng: GPM at a record high — can it spread its wings?'

Aug 20, 2025 call Trans 'XPeng (Trans): Targeting New P7 as a top-3 BEV in the RMB 200k–300k range'

May 21, 2025 'XPeng: After the grind, time to soar?'

May 21, 2025 '(1Q25 Trans): Poised to lift off'

Nov 19, 2024 review 'After three tough years, is XPeng back?'

Aug 20, 2024 review 'XPeng: Chronic volume pain, finally a glimmer?'

Aug 21, 2024 call Trans 'Mona + exports lifted monthly deliveries back to 20k in Q1'

May 21, 2024 review ''Bomb' did not spill over; XPeng held up'

May 22, 2024 call 'Overall GPM to stay at 10%–15%'

Mar 19, 2024 review 'XPeng: Volume is the chronic pain; counting on Didi’s Mona'

Mar 19, 2024 call 'Expect Mona to reach positive GPM with steady 10k+/month'

Nov 15, 2023 review 'Mediocre results: when will XPeng’s next breakout arrive?'

Nov 16, 2023 call 'GPM to turn positive in Q1 (3Q call Trans)'

Aug 18, 2023 review 'XPeng GPM collapse? The last awkward step before rebirth'

Aug 18, 2023 call 'G3i residual impact to linger; GPM to turn positive in Q1'

May 24, 2023 review 'XPeng: results have cooled; when does it heal?'

May 24, 2023 call 'XPeng’s pledge: hit 20k/month in Q1 (Trans)'

Mar 17, 2023 call 'XPeng 2023: reform, cost-out, new models (22Q4 call Trans)'

Mar 17, 2023 review 'XPeng: a target of criticism — can it survive the crossroads?'

Nov 30, 2022 call '+50% overnight spike — what did XPeng say? (Trans)'

Nov 30, 2022 review 'Bad results, stock up anyway? XPeng still needs rebuilding'

Aug 24, 2022 call 'G9 and a B-segment 'Model Y' may be the last push (22Q2 call)'

Aug 23, 2022 review 'XPeng is still far from profitability'

May 24, 2022 call 'Q1 is when price hikes show and GPM rebounds (Trans)'

May 23, 2022 review 'Sales leader, loss leader — does the market still buy XPeng?'

Mar 29, 2022 call 'Channel down-tiering lifted the delivery ceiling (2021 Q4 call Trans)'

Mar 28, 2022 review 'Selling more, losing more — awkward or bold?'

Nov 23, 2021 call 'Exploring Robotaxi; another step up in intelligence? (Trans)'

Nov 23, 2021 review 'Poised to be the new-energy champion — how far from 'China’s Tesla'?'

Aug 26, 2021 call 'XPeng: rolling up sleeves'

Aug 26, 2021 review 'A healthy report card with a smart heart'

May 14, 2021 call 'XPeng Q1 2021 call Trans'

May 13, 2021 review 'Bad press vs. XPeng beat — which do you pick?'

Mar 9, 2021 call 'XPeng’s Q4 call was more exciting than the print?'

Live

Nov 30, 2022 'XPeng-W (09868.HK, XPEV.US) Q1 2022 earnings call'

Aug 23, 2022 'XPeng (XPEV.US/09868.HK) Q1 2022 earnings call'

May 23, 2022 'XPeng (XPEV.US/09868.HK) Q1 2022 earnings call'

Mar 28, 2021 'XPeng (XPEV.US/09868.HK) Q1 2021 earnings call'

Nov 23, 2021 'XPeng (XPEV.US) Q1 2021 earnings call'

Sep 15, 2021 'XPeng P5 super launch'

Aug 26, 2021 'XPeng (XPEV.US) Q1 2021 earnings call'

May 13, 2021 'XPeng (XPEV.US) Q1 2021 earnings call'

Apr 14, 2021 'XPeng P5 reveal'

Risk disclosure and disclaimer:Dolphin Research Disclaimer & General Disclosure

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.