XPEV (4Q25 Trans): Iron robot targets >1,000 units/month by end-2026 ---

Below is Dolphin Research's transcript summary of XPeng (XPEV) FY25 Q4 earnings call. For our earnings take, see 'XPeng: All buzz, no profits — can the 'Eastern Tesla' story still hold?'.

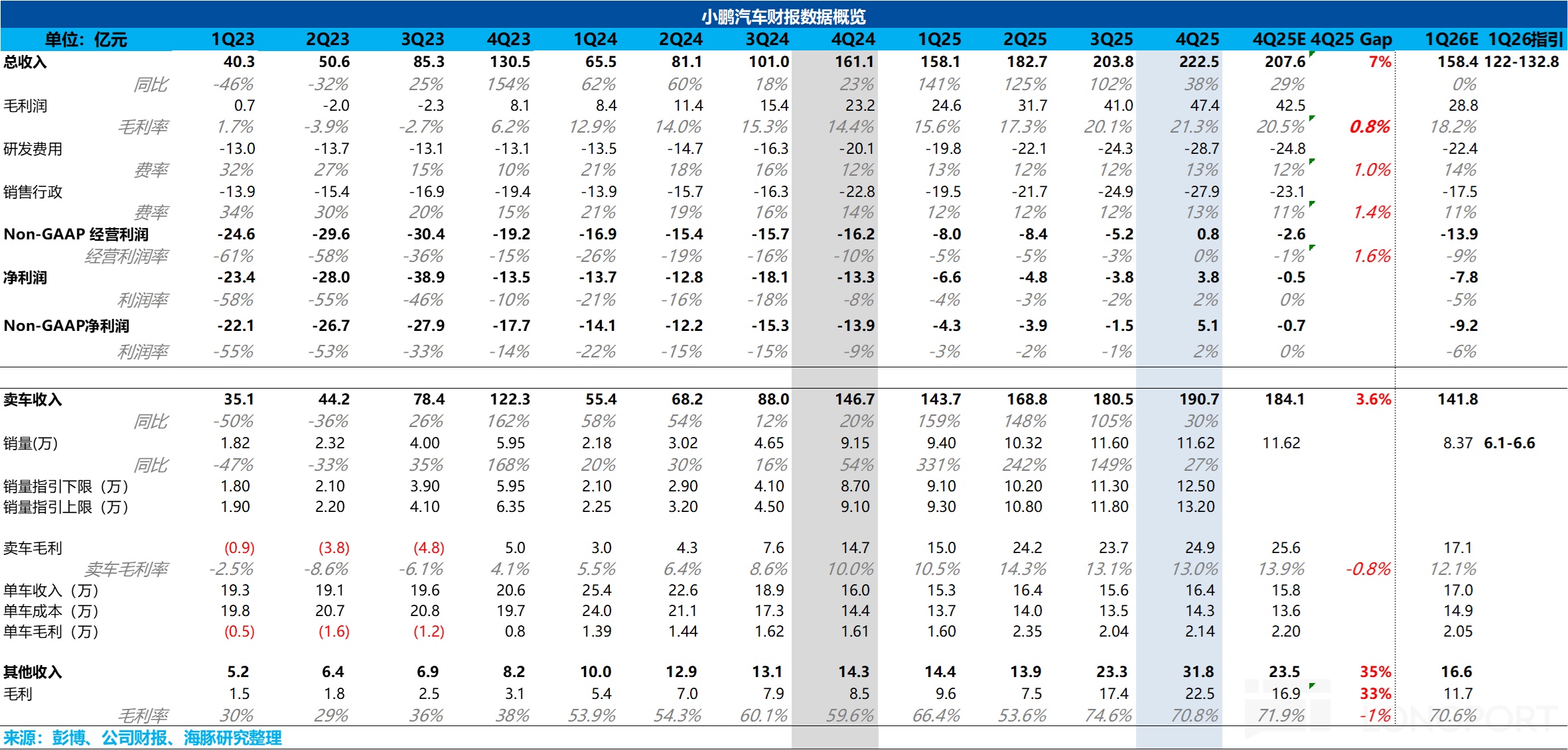

I. Key Financials Recap

FY2025 highlights:

- GPM: 18.9%, up 460bps YoY.

- Free cash flow: net inflow of approx. RMB 5bn.

- Cash on hand (year-end): RMB 47.7bn.

II. Earnings Call Details

2.1 Management Highlights

1) Strategy:

Positioning: The company is at a pivotal inflection for 'physical AI' applications, having built a full-stack in-house tech suite through years of hardware investment and a physical AI pivot. This stack spans SoC, foundation models, data, the WEE architecture, and AI infrastructure.

Outlook: Over the next 5–10 years, the physical AI market is expected to surpass autos in size. Smart EVs and humanoid robots both represent trillion-dollar global opportunities.

2) FY2025 progress and achievements:

Deliveries and sales: 2025 full-year deliveries reached 429,449 units, +126% YoY. This reflects strong scale-up across key nameplates.

Model performance:

- MONA M03 became the best-selling BEV sedan in the RMB 100k–200k segment.

- B7 Plus ranked No.1 among BEV sedans in the RMB 150k–200k sub-segment.

- Kunpeng range-extended EV X9 entered mass production, opening the 'dual-energy' era for a single vehicle.

- Overseas: Ex-China deliveries nearly doubled to 45,000 units, with Intl revenue contributing over 15% of total.

Technology and partnerships:

- Turing AI SoC entered mass production and began shipments to Volkswagen.

- VLA 2.0 (Vision-Language-Action) debuted, and humanoid robot Iron made its first appearance.

- Quality systems and NPS improved rapidly.

3) 2026 strategy, products and guidance:

Product roadmap:

New models: Four new launches are planned, covering large and compact segments on a dual-energy platform. They will support AD from L2+ up to L4 over time.

Flagship SUV GX: Pre-orders start in Q2 2026. This is a full-size six-seat SUV targeting a 'no-compromise, first-class experience,' offering MPV-level comfort and space with rear-wheel steering. GX will be the first model equipped for L4-grade hardware and software.

Design team: The team has been restructured. New models are designed for global markets.

Autonomous driving (VLA 2.0):

Progress: VLA 2.0 passed on-road tests in early Mar 2026, marking an imminent tech inflection and a generational lead. Rollout to users started in Mar 2026 and is ongoing.

Objective: The goal is to move high-level AD from an early adopter feature to a mainstream one. It aims to make AD a mass-market capability.

Iteration: The target is to scale parameters from billions to 20bn by year-end, lifting avg. miles per intervention by 25x and safety-critical miles by 50x. Full autonomy is expected in 1–3 years.

Testing and operations: GX with VLA 2.0 has a public-road L4 test permit in Guangzhou and is conducting L4 public tests. Pilot paid-ride ops are planned for 2H to validate tech, UX and the biz model, with overseas road tests for VLA 2.0 to start as well.

Turing SoC:

Performance and shipments: Since SOP in Q3 2025, cumulative Turing shipments topped 200k units. From Q2 2026, all MAX trims will fully migrate to in-house Turing SoCs.

Shipment target: The 2026 shipment goal is ~1mn units. This target applies to the Turing SoC.

External partnerships: Volkswagen is the first external customer for both Turing SoC and VLA 2.0. The company welcomes more AI firms, Tier-1s and OEMs to adopt Turing.

Overseas expansion:

Targets: Overseas deliveries are targeted to double YoY in 2026, with Intl revenue exceeding 20% of total. This underpins mix and margin.

Network and products: Four global models are slated for Intl markets, with a focus on SUVs. Sales and service outlets abroad are targeted to double from end-2025 levels to 680.

Infrastructure: The self-operated ultra-fast charging network will expand to 10 key Intl markets outside China. This supports ownership experience and utilization.

Long-term driver: Overseas revenue will be a key profitability driver. It is set to become a core earnings lever.

Organization: A major org upgrade merged the AD Center and Smart Cockpit Center into a General Intelligence Center. This marks a paradigm shift to unify driving and HMI on the same physical AI foundation models and infrastructure.

Humanoid robot 'Iron':

Mass production plan: The target is to reach mass production by end-2026. This remains the milestone timeline.

Tech capabilities: Powered by three Turing AI SoCs and the VLA 2.0 stack, combined with a 4th-gen motion control system. The goal is a generational lead in intelligence and motion control.

Use cases: Focus on commercial, industrial and household scenarios, with initial deployments in stores and campuses in China and abroad for reception, guidance and retail assistance. Ramp will proceed scenario by scenario.

Capacity build-out: A mass-production base for humanoids has broken ground in Guangzhou, with monthly output targeted to exceed 1,000 units by end-2026. This underpins scale and cost-down.

R&D:

- RMB 9.5bn R&D spend in 2025, including AI.

- In 2026, excluding vehicle development, physical AI-related R&D investment will increase to RMB 7bn.

Q1 2026 guidance:

- Deliveries: 61,000–66,000 units.

- Revenue: RMB 12.2bn–13.2bn.

- Outlook: As VLA 2.0 and four new models ramp, quarterly sales should trend up, with 2H YoY growth materially outpacing the industry.

2.2 Q&A

Q: Two questions on smart driving. First, what major VLA 2.0 upgrades are coming in the next few months? How will VLA 2.0 affect order conversion and user retention over the next few quarters?

A: For the first part, we expect at least one major OTA per quarter. For example, in the Q2 OTA, AD coverage will expand from mainly highways to small parking lots, campuses, communities and various parks, marking a shift from navigation-assist to broader area coverage. AD will also become more AI-agent like, and this year we will push more upgrades, including scaling on-vehicle or edge-side model parameters from billions to 20bn, targeting a 5–10x improvement in miles per intervention. Beyond AD, we will add multi-language support, helping integrate the cockpit with AD.

VLA 2.0 started rolling out to users yesterday (we began promotion in early Mar), and market response has been very positive. Test drives at our stores more than doubled QoQ, and sales of Ultra and Ultra SE also more than doubled. As VLA 2.0 scales and iterates, we expect higher volumes and conversion, and ultimately a lift in ASP.

On retention and usage, speaking personally, after experiencing VLA 2.0, it feels indispensable. The smoothness and reassurance it provides are unmatched. I believe AD will become a daily necessity, with usage potentially approaching 100%.

This represents a new paradigm. Our current focus is resolving many safety issues, but since the second-gen VLA, the rules have changed. As we close gaps, we can devote more time to bolstering overall capability and global deployment.

Q: Second question also on AD. What is the rollout plan for Ultra models and VLA 2.0 overseas, and how will this expansion impact global sales? Can smart driving software be monetized?

A: We have begun preparations for VLA 2.0 testing. By year-end or early next year, we will gradually launch testing, gray releases and deployments across regions. We believe VLA 2.0 has distinct overseas advantages: its generalization is strong, and in multi-market tests we found VLA performs well even without real overseas road data. It also shows specific strengths on smaller or rural roads relative to some peers.

We have seen this in SE Asia and Europe, reinforcing our view that VLA 2.0 can deliver a high-quality AD experience abroad at lower cost. Our hardware is already in place, so in 2H we will be ready for larger-scale testing and subsequent launches. We are also considering upgrades or shifts in the overseas software business model for AD, where we see substantial monetization opportunities and have strong confidence in turning tech strengths into revenue.

Q: First question on robot ambitions and long-term strategy. Management mentioned a product launch in Beijing soon and mass production by year-end. Beyond that, what major milestones should investors watch over the next 1–2 years? Also, as you expand from smart cars to humanoids, what can be leveraged in R&D, manufacturing and supply chain?

A: To clarify, we did not mention Apr, but rather the second half of this year. On your question, last year many supply-chain partners asked whether the humanoid supply chain should follow automotive-grade standards, and our view is that automotive-grade is the minimum. A car typically has one engine that, if it fails, can cause an accident, while a humanoid has at least 70–80 joints, where failure of any joint can lead to signal loss and severe safety issues. So we treat humanoids at least at automotive-grade, and since early last year we have been developing to those standards to prepare for manufacturing.

In that sense, we are a very unique robotics company, applying the same high standards as vehicle development to humanoids. We do extensive in-house development across joints, torso and other body parts, from SoC to foundation models, from data to training for the brain and cerebellum — a very distinctive approach. We have chosen a highly challenging path, perhaps 10x harder than Robotaxi development, to achieve the highest-quality mass production. By year-end, our MP target is at least 1,000 units. I believe future auto companies will also be robotics companies.

However, one big difference from cars is that humanoids can derive a large share of value from software from day one — up to 50% — while hardware cost may start at only 10%–15%. Value creation takes time to scale. But the logic shares the same roots: from R&D, MP, supply chain and quality, to global management, supply, sales, marketing and service, there are many parallels between cars and robots, and our persistent in-house integration sets us apart. From elbows and hands to legs and feet, we pursue in-house or at least co-development, again differentiating us from other auto or robotics companies.

Q: Second question on robots — cost and pricing. After year-end mass production, how should we think about cost reductions? Should we expect external sales after MP starts?

This is a great question. On cost structure, humanoids are quite different from what we have seen before. There are three major cost buckets: hardware, R&D and operations. Hardware cost resembles autos, but AI-related R&D will be much higher than for cars, especially versus the past when Tier-1s provided rule-based systems and off-the-shelf HW/SW — that era is over. In operations, it is a different world as data varies by scenario, and deploying to a new scenario requires retraining the robot's AI.

There are two humanoid types: general-purpose and specialized. General-purpose is akin to university where you build transferable skills and general knowledge, while specialization in areas like investing or medical practice requires significant focused training. For MP, scale will continue to drive BOM cost down, while software and ops costs will be optimized by model and use case. Unlike many peers, our goal is not academic research but real deployment and commercialization.

We will enter commercial scenarios first, then industrial, and finally household. Commercial requires extensive whole-body motion control — our strength and an area where we lead. Industrial will emphasize dexterity in the hands and bimanual manipulation, which we are working on. Household is the most challenging for deployment, so we will move from commercial to industrial to home in stages.

Q: First question on overseas expansion. Which markets will drive 100% growth abroad this year? Looking to 2027–2028, what products or tech will propel further expansion, and when will Kunpeng range-extended models reach overseas?

A: We started globalization in Europe, which is now our largest region, about 50% of overseas volume. Our premium-positioned EVs lead their segments in several countries, especially in Nordics, and we see encouraging growth in Germany, France and the UK. Europe will remain a key focus. After Europe, SE Asia was a major growth driver last year, with strong momentum in Thailand, Indonesia and Malaysia, and it will remain a key growth area. Beyond these, the Middle East, Central Asia and LatAm are emerging markets with substantial potential, where we established a footprint last year and expect continued penetration to drive growth.

To accelerate, several levers are in play: first, we are launching more products tailored for Intl markets. We plan four new global models this year, complementing existing segments from entry to premium, with body styles attractive to Intl buyers. Second, by year-end we plan to introduce range-extended lines in select markets to address charging and range constraints that hamper BEV adoption. We are also stepping up localization, including partial local assembly in key European and SE Asian markets since last year.

We also plan to roll out smart driving tech, and with DCAS regulations expected by year-end or early next year, our VLA 2.0 could be deployed in specific markets in Europe and SE Asia. In parallel, we are building org capability, hiring, brand and marketing, and starting self-operated charging in certain countries. All these efforts aim to lift our Intl competitiveness and brand positioning. We expect overseas growth in the next 3–4 years to far outpace the company overall and to become a core profit center.

Q: Second question on AI investment and compute. As Mr. He Xiaopeng noted, physical AI investment will rise to RMB 7bn this year. What is our current compute, the plan for the next few years, and will investments be expensed in R&D or capitalized?

A: Given the long-term nature, I can only give a high-level response. Over the next few years, automotive R&D will converge and stabilize, while AI investment will gradually increase on an upward trend, reflecting our conviction in AI. However, R&D will become more efficient, so in subsequent years AI R&D growth will not be as aggressive as before. Major investments will span AD, smart cockpit and humanoids, with increased spend as humanoids enter MP. All of these will be expensed as R&D, not capex.

On compute, no one can precisely define long-term requirements for physical AI yet. We currently have several thousand GPUs, and we think at least 100k GPUs will be needed for physical AI training at scale. We believe training cost and compute for physical AI will be 1,000x that of digital AI, and humanoid training will be 1,000x that of vehicles. We expect new methodologies to address compute constraints and infrastructure, including power generation. These are long-term challenges for physical AI, but we are confident in finding solutions.

Q: What is the status of current testing? What are the key milestones and timing for safety-operator and no-safety-operator phases in the robot business?

A: On software, we think fully autonomous capability will be achieved in about 1–3 years, not only in China but globally. Hardware development is on track. The remaining work is regulatory — securing permits, transitioning from safety-operator to no-operator, and additional R&D for global ops. We aim to start safety-operator test driving in 2H this year and target no-operator driving early next year. We plan to open the system beyond China, partnering with reliable global operators to provide Robotaxi or autonomous mobility services using our platform, tech and products.

Robotaxi scale-up and deployment will depend on regulatory progress, and all parts of this ecosystem must advance quickly. As for vehicle form factors that will support Robotaxi, there will be considerable exploration in the next few years. Fundamentally, we need to determine whether Robotaxi should be driven by cars or by robots, and clarity should emerge over time.

Risk disclosure and disclaimer: Dolphin Research Disclaimer and General Disclosure